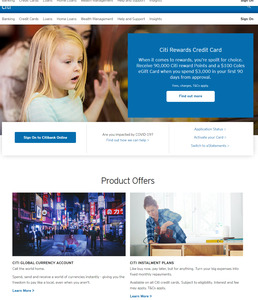

Citibank back at it with the churn and burn offers.

$2000 is a comparitively small spend for $600 cashback ($450 net profit after annual fee)

Added bonus of Priority pass lounge access.

Once again no cooldown period is quoted in the T's & C's, classic Citibank

Balance transfer rate 0% p.a. for 6 months2 with no balance transfer fee. Reverts to cash advance rate. Please note, no interest free days apply to retail purchases while you have a balance transfer.

Annual fee $150 in the first year and each subsequent year if you spend $48,000 on eligible purchases or cash advances in the previous year. Otherwise $300.3

Additional cardholder fee $0. You may have up to four (4) additional cardholders, who must be 16 years or older.

Retail purchase rate 21.49% p.a. or pay off eligible purchases at a fixed interest rate over a set term with a Citi Instalment Plan.^

Cash advance rate 22.24% p.a.

Interest free period Up to 55 days interest-free on retail purchases (unless you have a balance transfer).<

Minimum credit limit $10,000

Maximum credit limit $100,000

Good deal. The Apple/Google Pay requirement is pretty annoying though.