Interest rates are on the way back up again… after AMP dropped interest rates last year.

From 01 February 2022. Subject to meeting minimum deposit in prior month. Interest paid within first 10 days of new month. So if you wanted this deal, transfer $250 into your AMP account to start this from February (you won’t get any interest payment in Feb, but you will from March if you transfer $250+ In Feb).

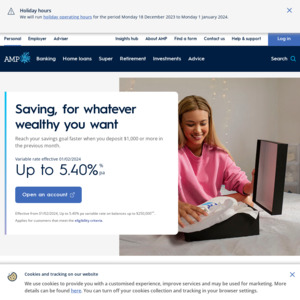

Terms:

Up to 1.35% pa1 variable rate on balances up to $250k. Rate is effective from 01/02/22 and applies for AMP Saver customers that meet the eligibility criteria in Jan 2022 with the interest payable within 10 days of the month of March.

Note in the past AMP interest rates have changed with minimal notice, so be prepared to shift your cash elsewhere if they change their minds.

i suppose you can churn the $250 in and out monthly?