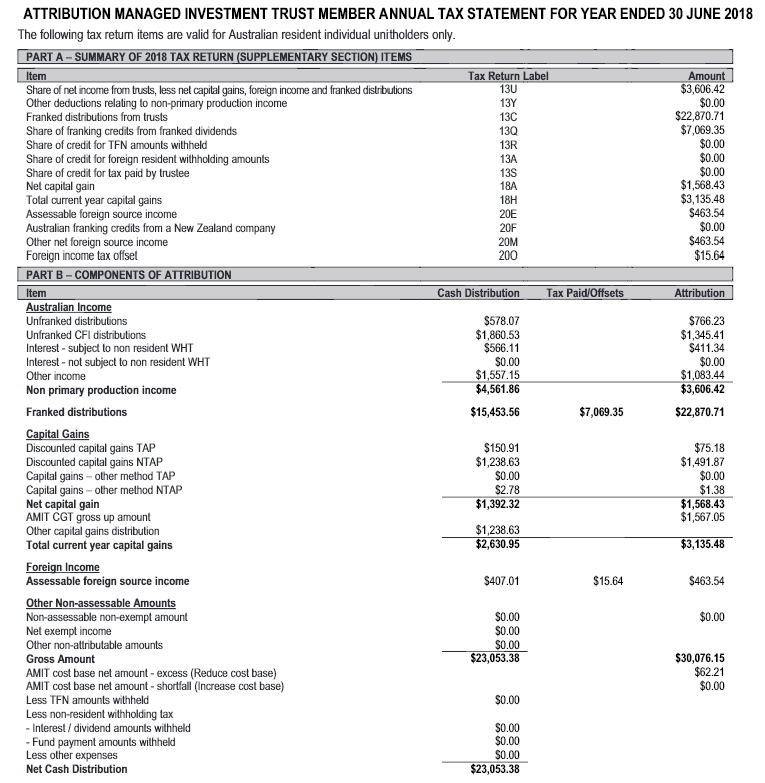

I invested some money in ETFs last financial year. This is my first investment in ETFs ever. I purchased IXJ, NDQ and ETHI via CommSec Pocket app. Now that I am collating all the information for filing my tax returns, I went online to check if my tax statements are available.

It turns out that IXJ is managed by Computershare and the only documents I can find after I log into my Computershare account are the 2 payment advices for the distributions they made in the last financial year. There is also an option to purchase a tax pack, but that comes at a whopping price of $49. I found a consolidated statement on CommSec but they state that their EOFY statements are summary documents only and cannot be used for taxation purposes.

So here is my question to you - In the case of IXJ, do I have to purchase the tax pack for $49 or is there another way to get the tax statement?

Additionally, can someone also confirm if I need to include distributions for June 2021 (as income) even though they were technically paid out in July 2021. I definitely need to include distributions for December 2021, even though it was paid in January 2021 because that still falls with the same financial year.

Thank you!

{kind=link}

What about NDQ and ETHI? I know Betashares send out a tax statement for their ETFs. I think it might be mandatory for all ETF providers.