https://www.news.com.au/finance/economy/interest-rates/fabul…

News reports say the very next day phillip Lowe lectured Aussies to work more and spend less.

https://www.news.com.au/finance/economy/interest-rates/fabul…

News reports say the very next day phillip Lowe lectured Aussies to work more and spend less.

Isn't that a BDSM group that meets once a month?

First Tuesday of each month except January?

Francis Dashwood and the lads. I used to live a couple of miles from West Wycombe.

Sex Cauldron? I thought they shut that place down?

Just cause you didn't get invited… :P

…more importantly….did they tip and if so how much??

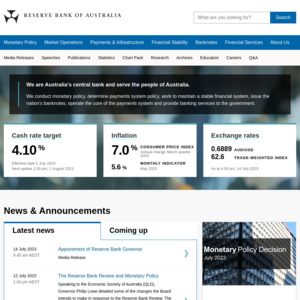

75 basis points.

Take the interest rise or double it and give it to the next person

Lol 250 guests divided by 25k.

But if they were served Vegemite sandwiches on ALDI sliced bread that is at least 300 sandwiches each, assuming the venue was free, they made their own sandwiches, had no serving staff, cleaned up after themselves, brought their own knife and plate and sat on the floor.

Fat cats!

ALDI sliced bread

Then you would have had a Dick Smith rant on offshore profits…

Dick Smith is too busy in cahoots with Kochie selling crypto on every single website i visit. No wonder Kochie retired from brekkie tv, must have his hands full with the side gig

@eggboi: Tricky Dickie is also feeding a protest group outside some foreign owned mines.

And his older girl is screwing big times with American ultra rich travellers!

Equals 0.01

It’s says in the article $176/head.

That’s wedding pricing territory.

It’s about $100/head?

The article says ‘140 VIP guests’ and I’m only quoting the $176/head from the article.

I’m amazed at how many people in this thread don’t seemed to have opened it

@ColtNoir: People are upset that the RBA spent $176/head for 140 VIP guests??

That honestly sounds pretty cheap.

@buckethat: It’s a bit on the nose when you’re raising interest rates to reduce spending in the economy.

‘We need people to spend less money’ and then proceeds to spend $25k the next day.

To me, I’m not bothered by the cost per head, I’m bothered by the hypocrisy of his statements accompanying the interest rate rises.

@ColtNoir: Yeah fair enough but these corporate events happens all the time, regardless of how the economy is at the time.

‘We need people to spend less money’ and then proceeds to spend $25k the next day.

I know this is semantics but this was very likely planned months in advance.

Companies/orgs spend money on frivolous events all the time, govs are notorious for how inefficiently they use tax payers money.. I just don't think this event in particular is something to be so up in arms about.

That’s pretty cheap head. The girls in Kings Cross even charge a bit more than that.

Don't you mean 25k dollars divided by 250 guests to get how much per guest

No because dollars are people now, and humans are the currency. Just ask the Fâṯ Čàṯś(tm).

Do you mean the other way around?

Punishing Hardworking Australians

Didn't punish me. But I guess then your headline answers my question.

Seriously though - increases in interest rates are necessary. We have suffered through Stevens's pumping of the housing market. Lowe has simply restored them to a modest level.

It would be great if government stepped in and improved housing for everyone by building significantly more public housing, improving taxation, improving infrastructure, cutting red-tape and dismantling some investment concessions. I would say the chance of that happening is between zero to two percent - regardless of who won/wins government.

In the meantime, the Reserve Bank remains most people's only hope. Lots of talk about those suffering through the rate hike: kind of surreal given the absolute silence over the past 15 years of those suffering through the rate cuts.

Not really mate - in fact, the latest inflation figures vindicated him on his decision.

You need to understand that inflation is dangerous once it's embedded in peoples minds.

So are super profits. If an industry gets it "embedded" in their mind that the expected margin is 30% when it was 15% last year, they would rather burn the world down than let that margin fall. The classical model of profit being the residual of spending and labour productivity breaks down when you start dealing with necessities of life combined with regulatory capture.

@brandt: Don't necessarily confuse busy and prices going up with profits. There's certainly not super profits in my industry - construction. Most construction companies making low single digit margins, or losing money and going broke. Inflation hurts head contractor builders more than anything (except maybe government red tape, actually possibly even more than this, except when its combined with inflation as we have now). We needed RBA to put up rates sooner so when we price / quote work, and then some time later are trying to finish that same project, can cover costs with our quoted fee…instead of struggling to get anyone to do the work and everything costing more and more every time we try procure something or someone to complete it.

Yet we can't seem to convince clients they need to agree to contract terms that reflect the time value of money (inflation) risk on them, nor can any of us convince anyone to pay ~7%+ more than what everything thinks something is worth now because that is what it will be costing when completed in a year's time. Had another example this week - a client thinking it was unreasonable for us to put prices up 8% for a job we won't complete for months (which in total will add up to just over 2 years from when first quoted when he first considered building it to the projected end date). That's despite that only covering just one year's price rise, when compounded with another for the two years that pass by completion, it should really go up circa 14.5%+, which means we are more than likely losing relative money, tightening margins to soften the blow and convince them to proceed, yet we were apparently the a…hole who was putting prices up, ripping them off, according to how he reacted. Then add to that the price was originally based on historical data from previous jobs (i.e. from the previous year to that when inflation was less important), and therefore probably not even reflective of what it was going to cost at that time quoted let alone the inflation since, and in reality you could be well in excess of 2 years out of whack from cost data that formed the quote to fixed price pay day… then consider things like government changing rules or imposing conditions that make things more expensive, and most importantly taking way too long to approve things or upgrade infrastructure despite you paying for the upgrade, meaning it is delayed more and the disparity gets larger… that's why inflation sucks for making some types of businesses work.

Don't forget, as much as they mismanaged the rhetoric back post COVID in unchartered territory, the RBA aren't creating the inflation (anymore), they are trying to slow it based on real world figures of inflation that are in many cases (e.g. CPI) far higher than the cash rate - figures that they didn't make up, but have to respond to.

I'm guessing there are plenty of small businesses not making super profits also - there's plenty of two-speed economy factors going on but they've only got one blunt instrument to put the brakes on.

@brandt: If margins go up, so will competition (assuming low barrier to entry) which will compress margins.

Yes evidence is showing margins are higher now, but that’s because the community has accepted inflation is high and therefore they’re accepting higher prices. Companies are pushing it as far as they can after long periods of very tight margins and strong competition. Stop buying and they’ll compress their margins.

@brandt: Unfortunately not within the remit of the RBA, and those who are responsible have been quite happy to tax the working population and give tax cuts to business. Australia now has one of the highest ratio of tax from individuals in the world.

The argument for the stage 3 tax cuts is based around this fact, and is why even the ALP supported them

So are super profits. If an industry gets it "embedded" in their mind that the expected margin is 30% when it was 15% last year, they would rather burn the world down than let that margin fall.

You just described our house of cards property market and the million measures in place to try to keep it propped up.

Firstly, let's be clear this is the decision of the RBA board, not of a single person - even the board's chairman. (No matter how some want to paint him)

Secondly, I would agree that the effectiveness of using monetary policy (interest rates) to control inflation is somewhat inherently unfair given the polarity of loan sizes for much of the population - with a smaller subset (with large loans) taking on much of the pain, with only ~30% of homes mortgaged at all.

However, the RBA does not make the decision on how to fight inflation. It is legislatively required to keep inflation within a specific band, and the only mechanism it has is interest rates. If something needs to be changed regarding how inflation should be fought, or the method of achieving it, this needs to be investigated by the parliament/government.

There are definite signs that perhaps the increases so far may have done enough, but equally there are other signs which show the opposite. Because of the delay of monetary policy's effect on the economy, and the lagging measure of inflation, nobody will be sure where we are for 4-6 months (and by then things may be much worse… or better).

not of a single person

I honestly cannot stand how much they're attacking one bloke. Like sure I get that he's responsible but I feel like if something goes wrong they'll just scapegoat him and then say "problems fixed" as if he worked in isolation or something.

He is already going very slow, skipping a rate rise earlier this year, and raising rates well below inflation.

The level of private debt we have accumulated makes rate rises more significant than they were in the past - a fact published by the RBA themselves so they are well aware

Didn't punish me.

Philip is that you?

I wish! 😁 I could definitely use a million bucks a year.

Crazy how people think property prices are normal.

$1m for a house 40 mins from Melbourne CBD isn’t normal. People don’t think about what their dollar is worth anymore, they just follow the market like sheep.

The norm isn't static. What was normal 10yrs ago wasn't normal 50yrs ago. Affordability defines the norm.

Disagree, people thinking a million dollars is nothing these days is what defined the norm.

As an example two bedroom units in Epping NSW were going for $800k a couple of years ago. If you think that’s value for money or if you’re willing to pay that you’re a fool.

@Ghost47: As an example, a 10-bed house in Strathfield, NSW went for $1.83mil 21yrs ago during the housing rout and everyone thought the buyer was a "fool". Put simply, words like "normal" and "fool" aren't words astute investors would use. If things always revert to the previous norm, then nothing would ever change.

@mun4: I would not compare a mansion in Strathfield on its on block of land to a unit in Epping that’s part of a low rise building.

I also disagree that affordability is what defines the norm, I would say willingness to pay is what defines the norm and if you think everyone makes sound and logical decisions when it comes to property I’d say you’re wrong, because humans aren’t infallible.

If I’m saying that property prices are silly, and you’re trying to say otherwise wdoes that mean you think that properties are priced fairly or logically? Do you realise what kind of issues we have and will have as less and less Aussies own their own home because they’re priced out?

@Ghost47: You're missing the point. Whether it's a mansion or a unit, it's still property asset. A "fool" buying a mansion isn't any less of a "fool" if they were to purchase a unit. The purchase price was still outside the so-called "norm".

I'd argue willingness to pay defines the price but not the norm because norm by definition is sustainable - a trend. Affordability itself isn't a logical concept - it's just a person's ability to buy. But if the price people are willing to pay stays high for long enough, then it becomes a trend and arguably becomes affordable as more and more people are able to buy at that price. They may have to cut back on other expenses, but they're still able to buy. In the past, the affordability test real estate agents ran was like 30% of income, but now it's around 40-45%.

The price of an item could be both silly and normal. Is Bitcoin at USD$20k silly? Lettuce at $4?

I would say willingness to pay is what defines the norm

So this is the norm then because this is what people are willing to pay for a particular area. The lack of medium-high density living in a city as populated as Sydney is why dwelling ownership is at a premium. There are plenty of other places where the median Australian isn't priced out from owning a dwelling to live in.

@Ghost47: It pains me you were downvoted on this. I agree, $1 million is a lot of money and a hell of a lot to hand over for a two-bed two-bath apartment in Australia.

@I like freestuff: If you don't consider it to be a lot of money, want to give me or donate a million dollars to a charity?

If you accidentally dropped a $100 note on the street, would that frustrate you or would it be like losing $1 in the couch cushions?

@Ghost47: It used to be someone would be flat out earning $1m over their entire working life.

Now a couple of 18 year olds can be on 100k each after 3 years in government jobs and could have more than a million saved in less than 10 years now if they tried.

@Ghost47: $1M isn't much these days and supply / demand is king.

You have to take into account that Sydney is a sought after city and people earn a lot more than previous generations.

For example, my parents didn't even earn 10% of what I earn and they bought a house.

Not everywhere costs what Sydney costs so there are properties available for a lot of budgets.

The issue is that many want to drive a Ferrari but they can only afford a Chery.

You are right, the dollar value isnt static.

however in the past a house was 3x yearly income. now its more like 10-12x.

that's not sustainable.

it is time to inflation the boomers early adopter advantage away. wages need to rise 10% a year for a decade or so.

@Antikythera: One factor is that in the past mortgages were normally only serviced by one income, now it is two or even more.

@Antikythera: In the past, population was smaller, the economy was smaller, and most importantly, fractional reserve banking has allowed banks to hand out debt like candy.

isnt this the key right here? house prices need to fall, wages arnt going up much to catch up, this housing mess has got us here and its gone take a decade to correct, this is just the start, much more pain will be felt for the last 2 decades of hyper house inflation to normalise.

People, especially those who already own houses are loosing grasp on how much $1M actually is, especially to those on the median wage and below (which by definition is most people).

Genuine question: wouldn’t the same amount of land (as your $1m melbourne house), 40 mins from any other first-world capital city, be worth the same if not more?

As in, its just because we all still want single storey houses on blocks of land with a backyard that makes it look exy. In other parts of the world, everyone’s been living in apartments and townhouses for 100+ years

Honestly it depends on how much people are willing to pay for it IMO. For some people like someone wealthy from China $1m could be 0.01% of their net worth. But then people born here who earn above average wage but nothing amazing (e.g. $150k) would struggle to outcompete the Chinese person at auction because to that person spending $1m is like losing a $5 note.

This kind of thing leads to houses getting bidded up which then solidifies in people’s minds how much it [houses] might be worth because people say “well that guy paid $1m for it so it must be worth at least that”. Houses and land are what worth what people assign to it and is a function of how wealthy they are. The thing is though with how globalised the world is there are probably a lot of rich people out there now with some sort of business and plenty of them exist here and overseas.

And for the record I just said Chinese for the sake of it, they could be a rich person born here or an immigrant from a different country like India.

It would be great if government stepped in and improved housing for everyone by building significantly more public housing, improving taxation, improving infrastructure, cutting red-tape and dismantling some investment concessions

Look up the CbCR (Country by Country reporting) reform Labor have just enacted. The media are absolutely silent on this because it is major reform. No more hiding your tax figures through creative accounting - it's being heralded around the world as an incredible crack down on tax dodging.

To be honest, if Labor does manage to tackle international conglomerate tax avoidance, they deserve a round of applause. I was hoping that Labor would use the Greens blocking their housing package as an opportunity to upsize it and shift the blame to the Greens for anyone who said doing so was imprudent (in my view, it's not).

Greens policy on housing is imperfect. Not just the developments knocked back. But if government starts bidding on purchasing established houses to directly convert to social housing how on Earth can that do anything but push up prices?

That said, I am shocked by the suggestion on Insiders that some inside Labor believe sticking to its very modest housing fund is a winner. There doesn't seem to be a reputable economist anywhere who believes the fund is sufficient to tackle the scale of the problem.

After years of the media saying the ALP are terrible economic managers (and this opinion now widely believed as fact), they can't go ahead and spend the money that is needed on infrastructure and hope to be re-elected. Just look at the insane criticism the VIC ALP is getting for 'wasting money' on building trains that apparently won't be needed in the fastest growing and soon most populous city in the country. The media influence is responsible.

This sort of they can't do better/at least they're not Liberal chatter - cements anti-Labor voters and lends credibility to the media organisations that criticise Labor. I have no love for Victoria Labor after the extensive lockdowns and no clue about why other people do.

@markathome: If you are referring to my comment, I don't see how it puts the ALP in a good light being more concerned about power than the ideals their voters expect

@markathome: My view is to vote for a leader that wants to improve the country, not line their own pockets. I don't fanboy for any political party, and will criticise bad policy on its merits.

I can criticise VIC Labor for stupid rules in lockdown, like curfew, and arbitrary caps on the number of workers in an outdoor building site. I don't believe the whole idea of lockdowns is stupid, there was a pandemic after all, and to say they weren't necessary in hindsight is also not being honest to the information available at the time. Nearly 200,000 people died from COVID in Milan, a similar population to Melbourne, so I see that as the number of lives potentially saved. I was working in a high risk customer facing profession, and I respect that my life was worth more than 'the economy' (corporate profits).

Happy to discuss if people disagree on the merits of harm from lockdowns vs harm avoided, it is subjective. but not if people are going to deny facts and reality and claim that COVID doesn't exist or is harmless.

Currently VIC Labor are spashing out free cash for energy bill relief, no means testing, to anyone who applies. At the same time they have a budget deficit. This is poor budget management. However criticism is lost in the sea of unwarranted criticism, and this is ignored.

My point is people that criticise the actual investment in infrastructure that governments should be doing are ignorant and biased, clearly influenced by biased media and their facebook groups. if we just play along with these narratives we are going to have both major parties full of corrupt power hungry d*heads, as any potential leader who wasn't one would go work for a private business.

increases in interest rates are necessary

Not sure it's necessary or could've been avoided. But I'm sure a lot of owner occupiers like me would disagree with above statement- a jump from 2% to 6% within almost a year.

a jump from 2% to 6% within almost a year.

It was plainly obvious this was coming if you weren't giddy on the dizzying high of free cash. (Either that, or hyperinflation and complete economic collapse). 6% is also not really that high. In fact, given that our "fractional" lending means bank loans are essentially printing money, 6% seems far too low. What price would you put on the ability for somebody to print money and devalue everybody else's salary?

"I would say the chance of that happening is between zero to two percent - regardless of who won/wins government.". Welcome to the Uniparty. No matter who you vote for, you get the same outcome. May as well just embrace a overt single party system like China has. At least the Chinese government sometimes gets things done and sometimes does things that help the proletariat.

To people complaining about interest rates, try Argentina (97%) and Zimbabwe (140%). Those are extremes, but there are quite a few countires in the 10 to 30% band. https://tradingeconomics.com/country-list/interest%20rate

Well said.. Also, the biased media never highlights the fact that a lot of Aussies have been punishing themselves by borrowing like nuts for the last three years, speculating the housing market. Why didn't these people foresee the punishment when they threw 'borrowed' money in auctions beyond their means and cheered with joy when they won the auctions?

No mention of the real punishment to the young or poorer ever whilst the others hold five properties with most of them in profit and they still whinge about interest rate hikes as if it was going to remain 2% forever.. If people really feel it's a punishment, then it's not hard to just sell the property/ies and exit.. market is extremely hot even today. Be reasonable, folks!

Why do I get a vibe that the interest rate hits Australian harder than other countries even though ours is still the lowest among others?

Huge mortgage loans because house prices are so high?

In the USA almost everyone is on a 30y fixed rate, so interest change only impacts new loans and people moving house.

Not sure about Europe, but often they have higher population of renters, with stronger tenant regulations, so fewer home owner mortgages.

30y fixed rate? good grief, what's the best u can get here?

10y from the big banks. Maybe longer through non-traditional finance, but at a guess it would be very noncompetitive.

2 years ago there were people in the US refinancing at 2.5% for 30 years. Now they are in the happy position of paying a mortgage less than the rent would be, but they can't move house or their payment would double if they needed to refi at today's rates.

While this is good for homeowners, it does mean that interest rates are a blunt weapon in the US, disproportionately impacting home building activity and commercial lending. Of course, one person's blunt weapon is another person's "great, I'm not being hurt" weapon.

Few years ago a relative in Europe opted for 30 year fixed at 2,3% (currently this would sit at 4% for 30 or 3,47% for 10 years). Mind you that was when their banks had negative interest and in 2020 you were able to secure 0.45% variable / 0.5% for 10 years / 1% for 20 years / 1.2% for 30 years.

before the rate hiking cycle they were getting 30y fixed at 3%+-

People in France get 25 year fixed rates of ~1.5%.

The United States is heaven for home owners. 25% of detacted houses there are on blocks larger than 1 hectare. Everything is better and better over there.

except the guns, and getting shot… by the police.

It changes depending where you live. A friend's monthly mortgage in USA is almost same as mine but the house value much lower. Both purchased around the same year.

Also, she pays almost 3 times more than me on house insurance. She lives in a capital city.

However, if you live in a small town, you could get a house for $200 K.

From the title of this thread I could guess where the source article was from

wow, 25,000 x $1 tacos

$1 tacos - shouldn't that be a bargain post?

25,000 chicken fajitas.

or 25,000 x $1 pizza slices

And the Treasurer and PM spent more of that on consultants in a second.

Dont forget they also added to your financial misery.

Well this is why we should all be over the moon about the federal ICACs arrival. PWC et al, and big oil/gas tentacle investigation should save taxpayers a bit. I mean half of the LNP will leave the country, LOL.

The LIbs, no doubt, will do everything they can to gut,close down or water down the ICAC powers as soon as they get in.So hopefully the swamp gets drained early in the piece

half of the LNP will leave the country

The LIbs, no doubt

I love seeing these factual comments here on OzBargain.

It's my duty.

Here's another factoid. Boomers win again>

https://www.news.com.au/technology/science/human-body/massiv…

Looks like grandad will be supplying future kids, while the Zoomers shoot blanks. (Mother Earth says , TYVM)

ROFL

@Ghost47: At this rate boomers will probably inherit the widows of zoomer influencers & re-populate Straya,

with their super virulent seed, while the unvaccinated zoomers fade away to oblivion.

There, in the 4 story Byron mansions, they'll sit and chat by the fireside reminiscing about the Lowe (and low fertility) epoch that ended the madness of post covid ,5G sponsored,tinfoilism.

@heal: Yes good point. A few may stay behind and enrich the lawyers, of fail and take on a new career in number plate manufacturing. Best place for corporate gangsters

@Protractor: Wondering what your crystal ball will say about the 3 million dollar payment to Brittney Higgins? Will any Labor ministers be joining half the libs making number plates when the Australian Corruption Commission finishes their investigation?

People who think $25k is outrageously expensive for 140 people to attend a dinner hosting the state premier and top executives from several of Australia's largest companies seriously need to get out more. Sure it's not cheap, but under $200 per person including drinks is not that outrageous.

I mean even comparing the bill to personal finances is stupid. Sure $25k is a lot of money to an individual, but this isn't an individual.

No mention of the hellfire club?