And did it again

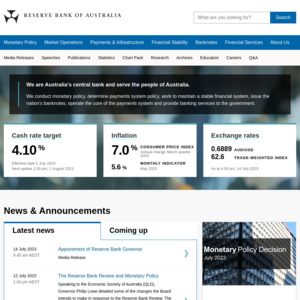

RBA hikes rates again increased the cash rate by 25 basis points, bringing it to 4.10 per cent.

rba #philliplowe #mortgage

What’s your thought ?

I see that There will be people selling their house and some becoming homeless

And did it again

RBA hikes rates again increased the cash rate by 25 basis points, bringing it to 4.10 per cent.

What’s your thought ?

I see that There will be people selling their house and some becoming homeless

The funniest people are the ones who say they don’t want immigration but want their property to increase in value or want to pump rents up more lol.

Im not one of them. Quiet happy to live in a comfortable house that is worth as much in 20 years as the day I bought it.

I am more interested in returns on savings, cost of living, that sort of thing. Negligible interest rates were a stupid idea (while I understood the logic, it was foreseeable that the economy would overheat if the easing and low rates kept up).

The fear of 'poor' economic performance drives pretty average policy. The desire for consistent uptick in gdp is both unsustainable at the 3-5% mark and unrealistic. It's a crack we cant or wont wean ourselves off of.

There's nothing wrong with a lower gdp. There's nothing wrong with lower population and there should be more focus on productivity improvements, which governments and businesses are just ignoring.

100% agree with you

And we aren’t even close to slowing down…. 10% mortgages are far from improbable

let the madness begin

Ubank already said: High 5 mate!

And its parent's share price dipped deepest in a year.

Not sure where you are posting this to, apparently this site loves to defend philip lowe even when he's in wrong.

IMO though he should have been sacked a long long time ago, and banned from participating in Australia's federal banking, and monitory decisions. See a single post criticizing that lowe guy or RBA and you only see downvotes.

Lowe is doing what’s best for the economy mate.

The backlash is just a symptom of those addicted to cheap money, thinking that they’re millionaires when in reality they’re just an average joe that has not improved their skills or started some sort of amazing business like Bill Gates did with Microsoft.

Hating on Lowe is like a drug addict hating on the person preventing them from taking more drugs. It’s just that instead of drugs, people are hooked on cheap money. Nasty addiction.

Most people are not addicted to cheap money,

Most people just cannot afford to have $2/L petrol, $500/ week rent, $1400 increase in monthly mortgage repayments, or a $300 a week grocery bill.

Problem is they WERE SLEEPING in 2019, 2020, by not doing their job properly. AND NOW because of their so called EXPERTs decisions SO MANY AUSSIES are suffering.

Problem is they WERE SLEEPING

So many stupid posts ITT.

The RBA has almost no control (by design), they are the patsy. The model for money creation is what's making those people poorer. The interest rate is only changing when you and the other slow saps feel the pinch, it's not causing or fixing anything.

Maybe I’m lucky I grew up in a small town, 5br 2bath waterfront for 385k in 2018 already mortgage free in my late 30s. Traveled the world in the military while getting paid, free food and free accommodation.

My condolences

That stuff wasn't free. Tax payers paid for it. Plenty of them would argue we could ( should) have spent the money we have on military incursions in the last few decades WAY way better, on issues on our own turf.

Hard to argue, the military procurement process is woeful but that wasn’t my problem, I just had to operate the equipment we had, with my best mates, all over the world. Good times.

Win any wars?

@Juddwah: What a pointless waste of money on nuclear subs will be ay.. you probably have mates to pretend reassure that your war efforts were any use..

but social media has made it look useless, so you decide to come here and make some brag, but you’re just another useless vet

@Juddwah: Thanks for furthering terrorist org, but we havent had many terrorist lately in aus since the withdrawal from Afghan

@HangryCakeStore: It’s because they are stopping from immigrating to Australia illegally by the ADF, and you’re welcome.

@Juddwah: Or the media of military in Afghan conjures hate and radicalisation of muslims in Aus. Also this assumption is for all military personnel’s reading this

@HangryCakeStore: The Taliban media department? I don’t think the have much of a media footprint in Australia.

@Juddwah: Doesn't seem to stop the bleeding down of economies for the sake of pretending there is 'one'. Or creating one (or more) for >

https://www.ozbargain.com.au/comment/13857688/redir

This will not end soon. Labor govt just got back into office. They will not want to be the govt who

1. Put Australia in recession.

2. Collapse of the property market.

The government will just splash the cash to keep the market moving hot.

Yep.

Australians need to sell up so the 1000 people coming in a day can buy something.

YOU BEAUTY!!!

Still waiting for Lowe to explain how external supply factors or price inelastic greed are fixed by rising rates or that low income earners getting a wage bump suddenly makes electricity companies or ColesWorth change their mind about the cost of milk.

I "benefit" from this btw as a saver not a mortgager, nor am I in that pay rise group, but at this rate (of progress) he'll cost me my job before doing anything about utility prices or prices of essential.

Still waiting for Lowe to explain how external supply factors or price inelastic greed are fixed by rising rates or that low income earners getting a wage bump suddenly makes electricity companies or ColesWorth change their mind about the cost of milk.

Destruction in demand will do that. Destruction in demand engineered globally will do that and more.

This 0.25% rate increases are so frustrating. Increase it by 1% for another 6 months. Renters will start sharing houses. Property investors will crack under pressure and the floodgates will open! What a nice sight that'll be!

All these boom/bust cycles serve to do is consolidate wealth/ownership into fewer larger holders - same for business, same for real estate.

Yeah, there will be less property investors, but after the recovery there will be just as many properties held by investors, but they'll average portfolios of hundreds or thousands rather than a couple dozen.

when the increases started, i thought .. 0.25% what a dumbarse. just jump it by 3% and shock everyone and that'll have a much more rattly effect.

What flood gates. Immigration will take care of the demand side for years. Interest rates have very little to do with the rent that is charged. Demand for rentals does, if magically 100k new house hit the market tomorrow that would place downward pressure on rents even if rates went up further.

meanwhile in the corporate world "new record profit announced today at company X Y and Z"

Are they really increasing? If you factor in inflation, last years profit needs to increase by more than 7% to make it worth more than todays profit.

Just like someone suggesting that the higher rates are good for their savings, unless your saving, profit etc. is outperforming inflation you are going backwards.

There is nothing wrong with zero growth, infinite growth is impossible.

We crap on about climate change non stop, the single biggest factor in climate change is our obsession with never ending growth.

More people, more buildings, more energy, more food, more space, more everything all with finite resources

Not saying there is but in Australia with a growing population any profit increase for a retailer less then inflation is actually going backwards.

Mo money, mo problems

- Biggie Smalls

Nice! I can't wait for it to go to 20%

When its 20%, I can tell my grand kids…. "back in my day, our interest rate was 20%!" and I can't wait for them to say "sorry millennial, you're so out of touch, today's houses are 5 million not 1 million back in your days!" Then I hit them back, wait until you see what my parents paid…. 120k… HA

How is 0.25 a hike, it's a rise.

0.75 would be a hike

.

The media loves to sensationalize. Every rate rise is a 'hike'.

I've actually never been better off than I am now. Basically on minimum wage but saved during the record low rates, fixed my rate and prepared for whats to come.

I'm not denying we live in an ever rising cost of living situation but the ones struggling have to ask themselves if in some way they are to blame for their situation if only a year after record low rates they can barely afford to live…

Only a few years ago interest rates were at 4.5% - 5% and everybody managed to survive. And now nobody can afford to live? If you are struggling now I feel for you, as the pain is only going to get worse…

The last time interest rates were 4.5% to 5% house prices were up to 50% lower than were today.

Ok. My interest rate was 4.5% less than 5 years ago. Sure as hell my house hasn't gone up 50% in that time..

I'm not denying that house prices have gone up significantly but it seemed to coincide with record low rates. It seemed like people were willing to over-spend because of low rates.

This was never going to end well…

You implying house prices went up by 100% in 4 years?

We bought ours in 2014 for $430k. Recent valuation for a refinance put it at $750k. So for us, yes house prices have grown stupidly

@klonky: Oh sure. From 2014. That's 9 years and still not 100%. Mine went up 35% in three years.

100% in 4 years is what I disagree with. And I agree house prices are stupid, especially with the atrocious build quality in Oz

Just be like monky… tree is free after all.. ooh ooh ah ah 🐵🍌

Another day, another dumb post.

ok short

Its kinda funny that the forum on Ozbargain has so many people complaining about inflation (and then raging about immigration, Lowe, housing, minimum wage, the rich, energy prices…) when the very site is built on finding "deals" for discretionary spending. Perhaps the first thing to do is to stop going to OzBargain to be tempted by deals for things you dont have to have…

Truth burns

Prepare to be negged.

Free speech should be applied judiciously, and always to conform with the flock.

but my new $300 patagonia puffer jacket is helping combat climate change!!!

Every one please stop posting deals for a few months and see if we can get inflation under control.

another great day for the banks but terrible for every average aussie battlers

fortunate to have paid off my house (bought in 2014) at the age of 35 in sydney and avoiding this madness

Why didn't you buy your second property?

For what its worth:-

a) I think that there are at least 2 further hikes left in the tank

b) we will start to see significant numbers of distressed sales in the RMBS sector in the next 6-12 months

c) hopefully LGAs in Sydney, Melbourne and Brisbane are starting to get sensible on medium density housing, which will hopefully take heat out of the rental crisis, although it will take years for those efforts to bear fruit

d) I can't believe that banks are still writing huge mortgages to people who just scrape by on the current buffer. Even now banks are absorbing about 50pc of the hikes to compete with each other for new loans. Scary.

e) A per capita recession in the near term looks likely

f) fiscal policy is all one way - massive budget line items (the submarine project is the biggest budget line item in the country's history), stage 3 tax cuts - basically at this point the RBA is fighting a lone hand against inflation

g) due to overall relatively low levels of sovereign debt in Australia, I dont worry too much about the bond market, but still…

I see the next two years being a low, slow grind, unless there is a hard recession, in which case all bets are off…

stage 3 tax cuts are a joke, wipe them off the agenda asap

getting rid of them would impact me, but im not stupid and i can see past my own nose that its bad for the country

The Most Expensive Housing Markets Globally By “Median Multiple” (2022)

the top 20…

1Hong Kong, China – 23.2

2Sydney, Australia – 15.3

3Vancouver, Canada – 13.3

4San Jose, United States – 12.6

5Melbourne, Australia – 12.1

6Honolulu, United States – 12

7San Francisco, United States – 11.8

8Auckland, New Zealand – 11.2

9Los Angeles, United States – 10.7

10Toronto, Canada – 10.5

11San Diego, United States – 10.1

12Miami, United States – 8.1

13London, Uniked Kingdom – 8

14Adelaide, Australia – 8

15Seattle, United States – 7.5

16Riverside – San Bernardino, United States – 7.4

17Brisbane, Australia – 7.4

18Denver, United States – 7.2

19New York (NY-NJ-PA), United States – 7.1

20Perth, Australia – 7.1

https://www.bosshunting.com.au/lifestyle/real-estate/most-ex…

If Singapore and Tokyo are not on the list then this list is rubbish.

Bosshunting is a shit sauce anyway

Perth is expensive kek

Radelaide is expensive topkek

what next darwin is expensive?

Tokyo is actually not expensive compare to Sydney. Duno about Singapore.

Tokyo's house is not expensive compared to income. My family lives and just recently bought there.

Agree. I lived in Tokyo before and when I came back to Aus sveryone kept asking if it was expensive. It absolutely was not!

Tokyo might be expensive per m2 but it isn't that expensive to get a Tokyo sized place. A friend just bought a new 2bed apartment near Ikebukuro last month for around 600k. And with a 1% loan.

The downside is that it might depreciate because they don't like old apartments there.

I'm half tempted to take my shitty Sydney apartment deposit and just outright buy a house an hour or two out of Tokyo.

But what size? 30m2? You gotta compare apples to apples. No point mentioning absolute amount without a comparable metric. A median sydney apartment cost about $800k and its average size is about 100m2 (newer apartments are up to 138m2). Tokyo might be $600k AUD but much smaller apartments? So on a m2 unit cost, it is not cheap.

@KaTst3R: That's literally the first thing I said.

And the list you called rubbish was clearly posted as "median multiple" which negates all that anyway. It's about how accessible the local markets are to their locals.

The comparable metric I should have included isn't property size, but my friends salary. Which isn't far off enough from our own median to be noteworthy.

I've lived in tiny Tokyo apartments very comfortably, which would have driven me insane in Sydney. Property size is only one part of it.

By that metric a shack in the outback is the best thing money can buy.

Where is Monaco on the list?

Locked down a 12 month fixed rate in March…maybe should have extended that one.

1 year fix is useless, like putting one $2 chip on red at roulette. Why even.

20-30% or properties are paid by cash, so plenty of money out there…

The people in extreme distress probably shouldnt be in property in the 1st place. What gets me is developers targetting people with "own your own home with only a $5k deposit".

Imagine living your entire life and only being able to scrape together 5k and thinking you're ready to own a home.

Housing is a problem, but so are dumb people.

Well, to be fair, that's when developers release lots of land that are yet to title. So you pay $5k or 5% the price of the lot to block it in your name. You still have to pay when it titles. I have a good amount saved up and would still take that deal.

I see that There will be people selling their house and some becoming homeless

People already doing it tough, there are plenty of homeless people in my regional - Vic town …

Interest rates were always going to go back up post covid and 4-5% is about the norm. Why would people be so ignorant to not factor in this inevitable rise. Yes it's harder but I believe it's the excess going out and holiday cash that's taking a hit and less the food on the table. The bank would of factored in a considerable allowance on a million dollar property not just the basic wage big enough to cover it

Ppl have not only ignored the impacts of a pandemic, they seem to think that working WFH was always the norm, and now railing against conventional workplaces. There's a crunch coming soon, given how many layers of class conflict have emerged since covid.

"Looks like we'll be buying aldi brand for a few more months in the hope rates start going sick down" = everyone who's "struggling"

people who "dont" do 80% of their shop at aldi (if they have one near by) are throwing their money away anyway

Shhh.

Keep it down, or Aldi will become empty or Colesworth

💯 Wish I could upvote your comment more than once!!!

https://www.smh.com.au/politics/federal/the-economic-narrow-…

imagine a financial system were people need to lose their jobs and unemployment to rise is a key indicator to bring inflation under control

pretty shit

min wage rise :

bill works at a bakery owned by betty

bill now gets 8% more wage

betty now charges 8% more on everything to cover bills wage rise

rba lift rates to counter inflation such as at bettys bakery

betty now pays more on her business mortgage so puts price up again

bill now pays more on his mortgage cancelling out his wage rise.

be like bill and betty, live in a country where the government has no brains

instead of increasing tax free threshold for bill, and rejigging upstream ones so the overt ATO loses very little if any

Betty is a greedy bitch who goes broke

Bill and Betty are now both on the dole.

Good one Betty

Being on the dole and jobless both Betty and Bill are lonely and poor.

Bill messages Betty one day on Facebook Messenger from the library because he doesn’t own a computer and can no longer afford a phone bill.

Bill and Betty start to message each other more, their messages slowly starting to become sexual in nature.

Bill and Betty meet, but since neither can afford condoms, Betty falls pregnant.

Betty pops out a baby nine months later whilst they are both still on the dole.

Maybe we should rename them Jack & Dianne?

Or how about:

Betty had seen the greatest profit in her business in the current year

Betty understands that it is not financially savy for her business to increase prices yet again, so she partially absorbs the cost of increases in the minimum wage

Betty somehow has more customers buying her products as those customers were on the minimum wage and can now afford food due to this increase

Betty sees higher revenue as a result of this, but also higher costs from higher minimum wage. Betty's company profit takes a minimal hit but is happy because it is still doing well and her employees are happier too.

said no company who is on the ASX, NYSX, FTSE, etc

My firm's profits are up significantly, I've increased staff salaries +15% this year, and hired additional staff just recently.

I'm in finance and accounting with a pivot into AI, my firm manages many businesses and their books are looking better than they've been for a decade.

There's more money floating in this economy than there has ever been in this country's history.

You forgot to mention the toothfairy.

Oh my sweet summer child…

More like Betty loses some of her business and she lays off couple of their staff. They move back to a shared house in an outer suburb or with their parents. Investors in the inner suburbs feels the heat and reduces the rent to attract more people. Which puts pressure on outer suburbs to decrease the rent as well. Meanwhile some of the investors have too much out flow than in flow of cash and they start selling the properties which reduces the prices.

This is my take as a millennial:

I have a decent job/income and a fairly modest mortgage for someone who fairly recently purchased a house with a decent deposit.

And I got a fairly cheap and modest house in an average suburb. In Melbourne (and most cities) there's basically nothing available for under $500k.

Far from the narrative of being reckless or not considering future rate rise. This was at the front of my mind.

But, still….. I'm really starting to feel the pinch now.

What more could I do? Buy an apartment 15km+ from the city? If that was the case I would have just kept renting as no real returns on apartments.

It would have been great to be able to buy a house 10-15 years ago, but I was at uni/school then.

As for expenses, there's really nothing more I could cut down on.

I bring my own food to work every day, don't have weekends away, shop at Aldi and very rarely get takeaway.

I have an average car that I purchased outright.

I'm even starting to limit social gatherings with with friends, or just drive into dinner and not drink, because it's just another financial hit.

Or meet for a coffee instead of the pub. And having beers and talking shit once a week is generally much more fun.

I'm spending more time at home watching TV for sure.

Surely hospitality is taking a hit? I can't be the only one doing this?

I can cop a few more rate rises, but it really hurts and I'm eating into my modest savings.

How people with 1million+ loans and other various loans/expenses (cars, private school, credit cards) are surviving is beyond me?!

Surely the shit will hit the fan eventually for some?

I think politically, anything beyond 2 more rate rises will be unpalatable. But I thought that 6 months ago….

If that was the case I would have just kept renting as no real returns on apartments.

You're viewing property as an wealth vehicle just like boomers.

Every advanced country a significant population lives in apartments/high density and its completely normal. You save on heating, cooling costs, transportation. Houses near the city in big cities are always going to be 1 mil + going forward. It's simply economics and not a human right to live in that zone.

Increasing rates is good as it will push money away from property speculation and normalize prices. 4% Cash is rate too much, but do people really have such short memories of 7-8%?

I think you totally missed my point.

If property makes money that's a bonus, but not my primary focus.

My main focus is a comfortable place to live.

I have a young kid and don't really want to live in an apartment for the next 10 years.

I'm not criticising apartments, but what I'm saying is if I lived in one, I would rent it for the flexibility.

But actually what is your point?

My point is increasing rates is good because property prices will flatten and people won't be able to take on massive loans fueling speculation.

You can't get a 5% loan for investing in a index fund but could for buying property. The tables have turned now, no more brainless loan taking.

If you buy a 2-3 bed apartment for 500k and invest 1 mil in s&p 500 you can live comfortably. And no a tiny 100sqm plot of pavers and some grass doesn't count as backyard. This madness spamming small houses on tiny blocks just so people can "live in a house" is insane.

Good. Keep them coming.

Until the government actually addresses the inflationary pressures causing the issues (not sure how many times economists need to say 'stop importing economy'), this isnt going to suddenly stop.

Welcome to the Big Australia policy. Recession or bust.