And did it again

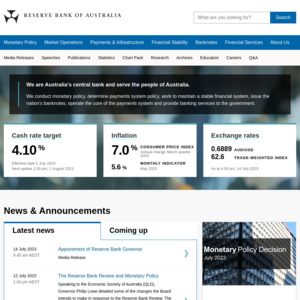

RBA hikes rates again increased the cash rate by 25 basis points, bringing it to 4.10 per cent.

rba #philliplowe #mortgage

What’s your thought ?

I see that There will be people selling their house and some becoming homeless

And did it again

RBA hikes rates again increased the cash rate by 25 basis points, bringing it to 4.10 per cent.

What’s your thought ?

I see that There will be people selling their house and some becoming homeless

No, that doesn't kick in until July 1st. Wages have been rising anyway, they were up 3.7% for the 12 months to the end of March.

Didn't stop business groups squarely saying the two are defo related.

We employ ~75 people in manufacturing business in Melbourne and staff are paid well above award.

However we will be increasing wages by ave 6% July 1.. if we don’t we will struggle to keep people as everyone is hunting and staff just hear pay rises are coming.. the expectations have been created.

RBA will be aware that most companies do staff reviews and salaries effective July 1 and this will boost inflation significantly.

Raw materials on many items are also repriced effective July 1 (we are still getting multiple increase notices daily).

Inflation will spike again.. sad reality unfortunately.

Inflation will spike again.. sad reality unfortunately.

I think we could see 8 - 10% interest rates in about 1.5 years' time.

What I worry about is the increase in crime, etc.

@whyisave: Don't worry about crime, as the same poiticians who EVERYONE voted for and created this mess, will also create a mess with reducing crime, and just lie about it.

Maybe people should reconsider who they vote for. Labor + Coalition + Greens are not the answer, they created this mess.

I think we could see 8 - 10% interest rates in about 1.5 years' time.

Care to post your modelling that lead to this view?

@SolitaryMan: I don't have any modelling for my thoughts.

It's just a feeling, for now :-)

( We can revisit this post, in 2 years' time! )

Also, looking at CBA's current interest rates,

it's already pushing 7-8% for a variety of their loan products.

I'm sure the banks don't release all of their modelling,

and trying to secure fixed-term loans at low 8s %.

The quick, easy (and benevolent) solution is a debt jubilee,

ie. for central bankers just to forgive country's debts

and bring about stability in the world.

It would have played a part I'm sure.

He is saying that he failed to control inflation like what they did in USA by consistently increasing rates at higher % … !

Yanks have long term fixed rate mortgages though.

Recent home buyer: "Oh no! I'm going to have to sell a kidney and eat my child now!"

Savers: "Yay! My savings will be going backwards slightly less a few weeks/a month/however long it takes for banks to raise savings rates."

Old people: "Stop complaining about 4%, we had 20% back in our day and WE LIKED IT!"

Economists: "Recession here we come! Woo!"

First home buyers: "BRING ON THE COLLAPSE BABY!"

Surprisingly few distress sales in the market.

My understanding is that the majority of fixed rate loans are coming off now until the end of the year. There should be a lot of distress properties coming to market in the next 3 to 6 months. Just imaging trying to find an additional $2216 more on a million dollar loan that is coming off a fixed rate. :(

@spiderext: Most people who fixed did so knowing that the rates then were too good to last, so they will definitely have factored in some sort of increase but maybe not to the extent it has gone up.

In fact, far from being the idiots some make out for believing Lowe's no increase until 2024 stuff, they didn't take his word for it and fixed anyway. If they believed him there would have been no need to fix in their eyes.

@Brianqpr: I fixed for 5 years at a little over 2%. I knew regardless of promises the rate wasn't getting remarkably better.

It was only a few months before the variable was above what I'd locked.

I factored in a safety net of around 7-8% increase after the locked peroid on my wage alone. My wife can earn as much as me, but will be stay at home mumming it for a few years when the baby comes along.

@spiderext: Heard this so many times. Usually from people who have very little understanding of how the banks work.

Working specifically in retentions, I can tell you that banks do not want your house if you cannot pay your loan and 99% of the time mortgage holders do not want to sell. The banks will do everything they can to help you work your way through. Even if you choose not to cooperate its generally takes about 2 years from the start to finish for banks to evict and sell you. They avoid it!

So if you're waiting for prices to tank when fixed rates come off, you'll be waiting at least two years and by that time rates will more than likely have reversed.

@spiderext: Fixed interest borrowers had almost 18 months to build buffers. And if push come to shove they can always re-fi onto interest only for a few years to ride out the high rate.

Even if they do go to sell, they'll make a profit, having said that, I'm not seeing ANY mortgagee sales at all in the North Sydney area.

@xavster: Can’t necessarily re-fi, especially if they borrowed to max capacity when cash rate was at 10bps, nobody will re-fi to the same level now.

Agree with your last point, very little supply in the area.

@spiderext: Yeah but they’ve opened the immigration flood gates for dirty/black money out of China and India.

@[Deactivated]: It’s funny how people get angry at Indians and Chinese for coming over when it’s the local businesses and Australian government that’s inviting worker over. If you think there’s black money coming over from overseas, be angry at your government for letting it happen.

Also a fact people conveniently ignore is that the top overseas buyers of properties are from the UK and NZ. Of course we don’t call them foreigners, how can we?! /s

@[Deactivated]: As someone who owns an accounting firm and deal in this area and have a lot of clients from China & India, you have no idea what you're talking about.

Exactly until this happens it's all just whining over nothing.

If you arent selling you arent hurting that much

First home buyers: "BRING ON THE COLLAPSE BABY!"

LMAO -if you couldnt afford a property in a low interest environment - you wont be able to buy one if property drops 10-15 percent because your borrowing capacity is like 40-50 precent less then before the rises

the only people who want a collapse are those who are 'cashed up' enough to hover up properties and other assets without having to take on too much debt….this rich people get richer hold on to assets poor people need and when the economy picks up they sell them to poor people at a huge margin

I know alot people at work who are on fixed heading off into the mortgage clift cant refinance due to risk.

One person has had their parents step in to help keep up the repayments and they are planning to move back in with their parents

@George Washington: that is quite sad but the smart thing to do, I know a few years back it was a lot easier to get a loan and now they have to assess at +3% the current interest rate. Even then with the ever-increasing house prices and not knowing what will happen real estate and interest rates are a gamble.

I know alot people at work who are on fixed heading off into the mortgage clift cant refinance due to risk.

One person has had their parents step in to help keep up the repayments and they are planning to move back in with their parents

i dont know a single person who is open to selling in this market - i know a lot of people who were or are in fix loans my reponse is if you were lucky/smart enough to fix till now then you hopefully would of been smart enough to build a buffer when the fix rate ends.

Im sure, some people will be 'forced to sell' but i dare say builders going bankrupt, lack of aread to build near the CBDs, Albo-fraud bring 1.5m ppl here, a dire rental market and the fact so many people have the bank of mum and dad will put way more pressure to push prices up or keep them stable.

If the market ever was to (meaningfully) crash it would probably need more then just high/higher interest rates it would need a negative property sentiment which i just cant see happening with this government (or even the opposition government in charge) - the very culture 'around' property in Australia is something i cant see changing anytime soon

Thus all these interest rates are doing are pricing poor people out of the market as prices seem to be stable (if not going up) whilst borrowing capcaity is dropping rapidly - ill also add this just because someone needs to sell that doesnt mean they will 'sell for a loss' as i mentioned above there is a lot of reason the market will remain elevated and the biggest reason is our current federal government it is no clue housing policy

@Checkmate3023: Yes prices will not drop in Australia, people will just withdraw their homes from sale and builders will cancel projects.

However interest rate rises have already had a significant impact on demand that will stop the pace of price rises (which is the best the poor can hope for).

Mate, I'm not cashed up, have a mortgage and I want it to implode.

@tessel: I think how i see it going is more people crammed into one home/unit and higher rents to support those mortgages.

Put it this way a workmate paid 890k in Blacktown just before the Ukraine invasion. paid 20% deposit i assume didn't fix as he was planning to shop around for cash back. Was living in it, now its on the rental market trying to ask for 600, still on the market. he still has a short by 3k for repayments.

He cant now shop around because he would not be able to meet the new assessment criteria. He said he is going to try his best to hold on and worst case his missus will help. He said onces he sells it will be impossible to buy back into Sydney.

I know how tragic is that!

First home buyers will be screwed in a collapse, if they cant afford now it will be even worse in a collapse as banks will severely tighten lending requirements

First home buyers will be screwed in a collapse, if they cant afford now it will be even worse in a collapse as banks will severely tighten lending requirements

sadly a lot of them are screwed i dont think their will be any 'correction' to house prices but i do believe some people who borrowed to their (or close to) their limit will be in trouble

@Checkmate3023: yep, what a lot of people don't seem to understand is borrowing capacity is not a 1 to 1 ratio for interest rates. each 1% rise in rates drops your borrowing capacity 7-10% from the current rate. they would need a massive massive drop in house prices to just be in a break even situation to today. 10-15% is not even close to being enough to cater for the rate rises we have already had.

They forgot the system is dynamic. If housing does collapse, the economy will most likely be in big trouble with massive unemployment. So first home buyers won't have jobs to take out a loan ;)

There will always be jobs picking fruit. Problem is most Aussie's are too lazy and backpackers and Islanders do it instead. People always need to eat.

@BluebirdV: too lazy or would rather not work like a slave in shitty conditions when they could be doing something else?

@BluebirdV: Just let the overseas ppl have that, as usual… they couldn't care any less, but yeah, in a decade I met a few "regular" australian workers.

Wont be any collapse, just more overseas buyers/immigrants and already rich investors buying more from first home buyers selling who can no longer afford it.

This does not benefit anyone except the rich. Class separation will just continue to worsen.

Better off money wise selling the kid and eating the kidney

Have you considered selling both and eating the money?

Not better off money wise, eating it.

Old people: "Stop complaining about 4%, we had 20% back in our day and WE LIKED IT!"

I actually wouldn't mind this if the property prices were what they were back then! haha

Give me a $30k house at 20% any day

Way back when Average House Price to Average Income ratio was 3-4:1 rather than 10:1 and university was free so no HECS to pay off.

Ignoring the fact that with the consolidation of wealth, the average income is like $40k p/a higher than the median.

@Sleeqb7: Way back when ppl didn't have $50K of gadgets in their rental while whinging about having no deposit?

How many ppl (% of population) were going to uni?

What was the population back then?

The rise of credit has allowed ppl to live way beyond their means and capacity, and the tendency of humans ever since to 'accumulate' shit has erased the old school philosophy of going without. So now, when real inflation and a pre -recession economy kicks in, a big swathe of ppl have zero tools to cope.

Plus population. There's too many of us (and not enough resources + massive ecological impacts) to maintain the temporary capitalist model in perpetuity.

@ajr5k: I have $50k worth of gadgets..

Reality is that after having paid the real necessities (food, shelter and clothing) we have a larger disposable income (as % of income) than any time since federation.

Appreciate this won’t be popular but it is consumerism that is making people poor.. not interest rates.

Appreciate that there is really genuine people struggling, but the majority really have consumerism plague.

Yes it will tighten up for a few years but it’s not like a period not that long ago when unemployment was 11.2% (1992) and we all knew someone who was unemployed.

Yeah it's easy to pay off a house with 20% inflation when your wage growth is at 20% as well. All that matters is that your wage growth is keeping pace with the mortgage interest rate, as long as that happens, you should smash out your home loan as your principle doesn't grow. Eventually, your income ratio will drop vs your principle and it gets paid off very quickly. Thus why we laugh at a $70k house because our average income is now $100k. That's why you don't see any home loans left unpaid for a $70k house.

Dude 20% of 100k house is NOT the same as 5.5% of 1mil house. Good grief …

Yes that's his point, boomers need this drilled into their skulls.

$100k 30,40 years ago is not the same as today's $100k

It’s the multiple of median income that needs to be looked at.

It was 4x then and 10x now.

So at median wage of $80k, house should cost circa $320k and not $800k or $880k at 11x.

Borrowing 90% with no LMI with a 30yr loan:

At 4x, Mortgage repayment on a $300k loan @ 20% would be $4813 per month.

At 10x, repayments on a $720k loan @ 6% would be $4317.

At 11x, repayments on a $792k loan at 6% would be 4748

@MakkhiChoos: I do not really agree with you on house price should be 4x because work and income structure is very different, but even by your calculation, at 11x @6% repayment is $4748 less with 4x @20% $4813

Update: They will need a 2nd job in order to maintain their [already] frugal lifestyle now

Those old people should shut the hell up.

No way would the majority of them been able to even enter the market if they had to pay today's prices. Not only did they live in a period of extremely low house prices, their interest rates were high because of rampant wage inflation and what was original a 3x annual salary mortgage became 1 or less. They could at their leisure have one working parent comfortably and had a huge backyard to play in with their kids which they could afford to have when they were all 20 years old!

Or hurry up and cark it so young people can have a fair go

I agree, their lives were essentially easy mode. They didn’t have to compete globally for jobs either.

'easy mode'? That's a bit rude, which easy mode are you referring to. The ones that spent their development years in the fallout of WW2, the ones drafted into Vietnam or spent theirs childhood listening to it. Those living through the cold war and imminent promise of destruction any minute or maybe the arrival of AIDS that was forecast to overrun the world and was unsurvivable. Things were just different, they had to save for retirement, no medicare, no paid parental leave. Job's weren't protected. White goods cost 12 months of disposable income. No cheap clothes or anything from Asia. So many things were different it's ridiculous to try and compare living standard by home price alone.

Even the standard of a home is so very different you can only compare land price.

Well inflation is still climbing, so that's what the RBA is meant to do. I bet massive credit expansion from people wanting to sprint up the property ladder doesn't help with inflation.

I'm not protesting in the street because I (an Australian) support the RBA's decisions. What's your excuse buddy?

sounds like something a communist would say!

Settle down there Mr McCarthy!

I support the RBA decision and I'm uber right-wing, conservative libertarian.

Next.

Lmao you might wanna look up the meaning of ‘communism’ General Franco

Yeah, the rates are not going high enough and the government wants to increase inflation. The crazy inflation of everything is eating up my wage!

Greens are not in government any more than the LNP are. This is Labor's show.

@[Deactivated]: You're forgetting just one minor detail.. 9 years of libs prior and a pandemic. But sure, it's all Labor's fault.

@DeToxin: im not on either side of the political spectrum…in fact i used to vote labor, but i can see why i dont any longer

@[Deactivated]: Not trying to be profound, just giving you a metaphor for your last two comments which are pretty contradictory

@DeToxin: Yes, Indeed libs messed up. But Labor is no less…who opened historic immigration tap in middle of rental crisis….

its always blamed on the current party. It would have happened regardless, our economy follows america, if they fall into a recession, we will also.

Labour

What does the UK Labour party have to do with the Australian economy?

LOL the LNP let the market heat up last nine years and somehow you complain about the last one year under ALP.

@burningrage: Selective memory you have. Weekend and holiday surcharges started appearing after Covid lockdowns were lifted. CC surcharge being an extra became a lot more common too.

Reserve banks across the world are raising rates, it’s not an Australia specific problem. FWIW the RBA is independent of the prevailing govt. so if you feel ALP is somehow forcing the RBA to raise rates, you can equally argue the LNP forced the RBA to keep rates artificially low for too long. Having the rates so low is the reason housing heated up so much. Lowe himself admitted that they should have started raising rates sooner.

@burningrage: You don't think see any connection between the the current environment and decade of cheap credit and subsidizing property investors?

Looks to me a decade of economic mismanagement that we finally have some adults in the room who can actually make the tough choices.

@burningrage: How oblivious can you be?

With govt debt tripling in their 9 years in power and ending with a once in a lifetime pandemic event you expect the situation to be all well and good in the first year of recovery?

You don't remember weekend surcharges because hospitality venues used to underpay staff regularly and food costs were low - now they don't want to risk being taken to the cleaners like old Georgie boy, and food/power costs are much higher.

@burningrage: I really can't understand how your thought process can be so limited. What do you think labour come in and hit a switch and everytning suddenly goes to shit?

Well if you work, don't take the wage rise or donate it to the poor struggling Italian suited corporate Mafia that is the Liberal Party.

Open your eyes, the entire planet is struggling economically. Good economic managers? Nah, just above arrange BS artists with the most gullible fan club going around

What 5 things? This cycle started before the election, is happening globally (including in countries with Liberal/Conservative type governments), and Lowe said only last week that he believed Labor's budget would actually help bring inflation down rather than add to it.

Greens aren't managing anything, Labor has a majority.

Stoopid reserve bank, I'll bet they are all vaxxed for covid as well.

welcome to the great reset…you will own nothing and be happy.

Cooker - confirmed.

Bad satire is bad.

im alright jack?….most arent affected. yet…

People aren't protesting in the streets but crime is going up… sharply. People pretending that this hasn't had negative effects live in a safe neighbourhood (for now). There's going to be a lot of home security deals and forum posts on here in the next few months.

here we go!!

Property prices and rents to go up again and again after landlords sell to home buyers (who else would buy??) and renters move to cheaper rent or go homeless.

Past 6 months make no sense.

Nobody is selling right now. Property investors are HODLing on in deluded hope that prices will continue rising forever despite people's savings, real wages and borrowing capacity being blown to bits. Watch them run for the exit in 3-6 months time.

We have a shortage on housing. Supply and demand would suggest more builders will wanna build. Except credit is restricted so no one can afford to build. It’s a mess.

Is he hinting at the recent minimum wage increment?