{kind=link}

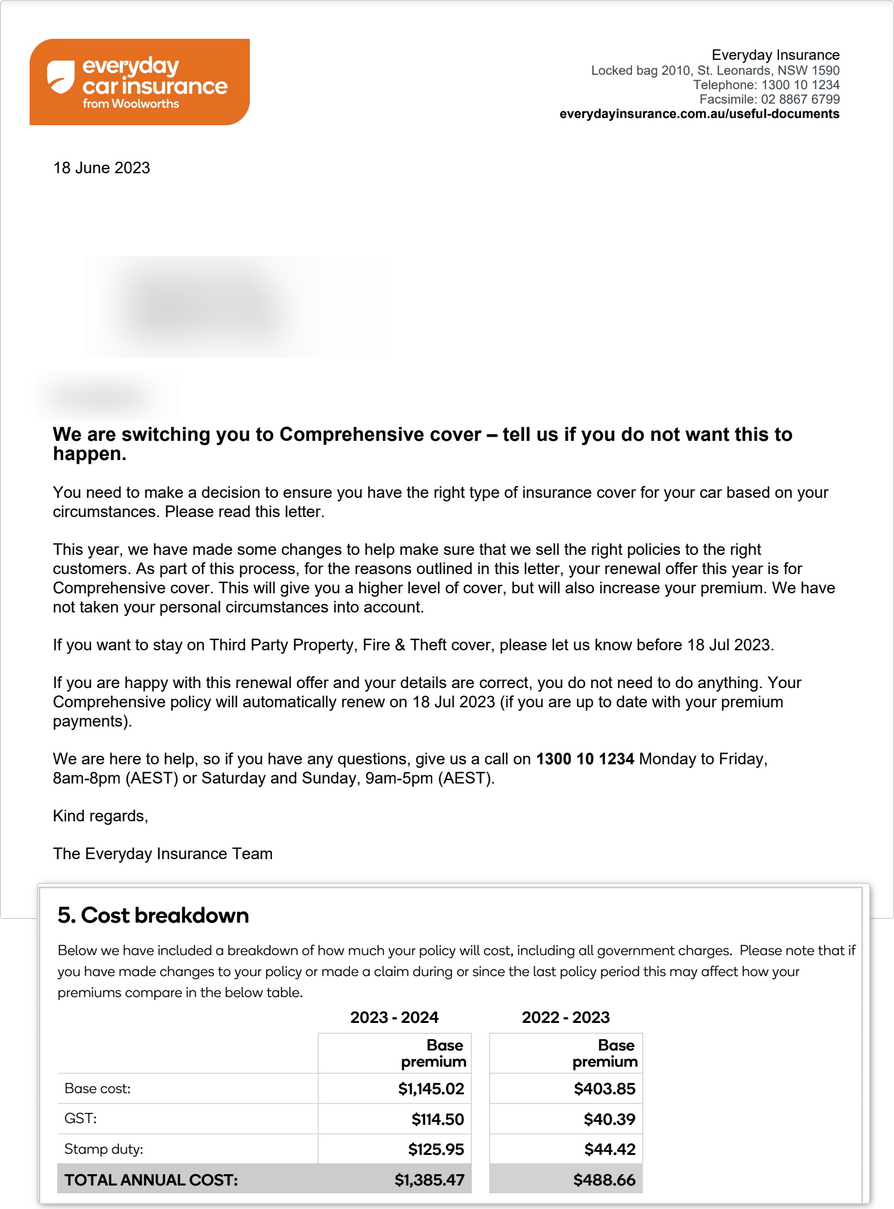

We are switching you to Comprehensive cover – tell us if you do not want this to happen.

You need to make a decision to ensure you have the right type of insurance cover for your car based on your circumstances. Please read this letter.

This year, we have made some changes to help make sure that we sell the right policies to the right customers. As part of this process, for the reasons outlined in this letter, your renewal offer this year is for Comprehensive cover. This will give you a higher level of cover, but will also increase your premium. We have not taken your personal circumstances into account.

If you want to stay on Third Party Property, Fire & Theft cover, please let us know before 18 Jul 2023.

If you are happy with this renewal offer and your details are correct, you do not need to do anything. Your Comprehensive policy will automatically renew on 18 Jul 2023 (if you are up to date with your premium payments). We are here to help, so if you have any questions, give us a call on 1300 10 1234 Monday to Friday, 8am-8pm (AEST) or Saturday and Sunday, 9am-5pm (AEST).

Got the above letter by Woolworth Car Insurance deciding to change my coverage should I not get back to them in time - raising premiums 3 times more than what I'm currently paying. Anyone else finds this absurd? Instead of them contacting me to ask me to consider increasing my coverage, they've gone ahead and put the onus on me to contact them to put a stop to a change I did not authorise from happening. In all my years on being various insurance, I've never encountered anything like this. I have never made a claim, ever, on my car insurance history nor have I ever had a claim made against me.

https://www.pictr.com/images/2023/06/18/EdRKJO.png

Anyone else finds this absurd? Anyone thinks this is some breach of some laws somewhere (to make changes without customer's explicit consent), especially considering this is a financial product? Are they relying on the % of people who don't scrutinise their bills and just let it slip through?

here let us upgrade your policy without your consent, you can thank us later……insane. find a cheaper quote & leave immediately