This will be available as from the 20th of April but you can register your interest now by logging in to your myGov account and following the Intention to access coronavirus support instructions.

Has anyone done it or planning to do it?

Is your situation so dire that you couldn't make ends meet without it?

JJB

Added a poll : Are you going to access your super? Why?

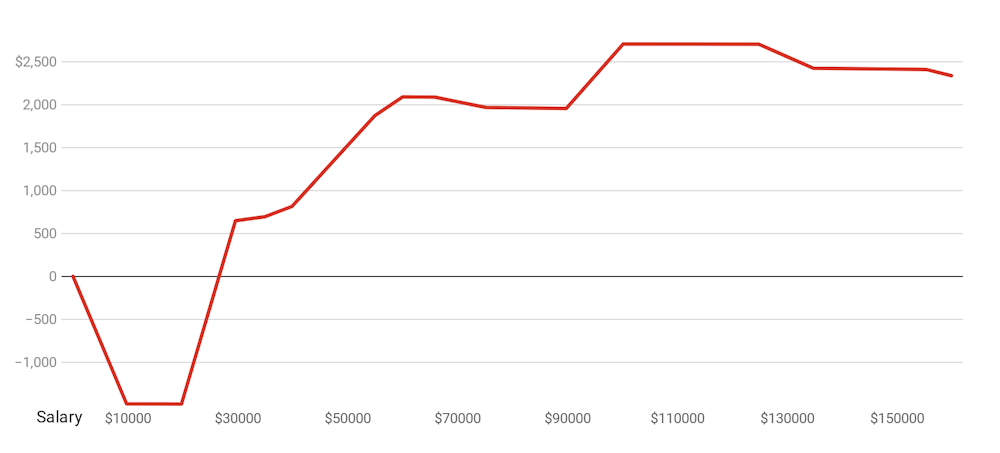

Edit: The tax loophole

To take advantage of the tax loophole, beneficiaries would need to fit into a rather specific cohort of earners:

- qualify for early release of super, which means having been made redundant in the coronavirus crisis or, in the case of sole traders, having lost at least 20 % of turnover.

- a working-age individual who is on 9.5% compulsory super contributions,

- has an annual salary below $158,000,

- has made no previous voluntary contributions to super in 2019-20, and

- who elected to make a “simultaneous” (within 2019-20) pre-tax contribution to and withdrawal of the maximum possible $10,000 from super over the next three months.

As long as an individual in this situation has an annual income of approximately $30,000 or more, there is a prospective tax saving from rearranging his or her financial affairs over the next three months.

{kind=link}

No. Terrible idea. Can't believe it's allowed.