Deal link goes to public product page because I couldn't work out how to submit this deal without a link - look at description or screenshot

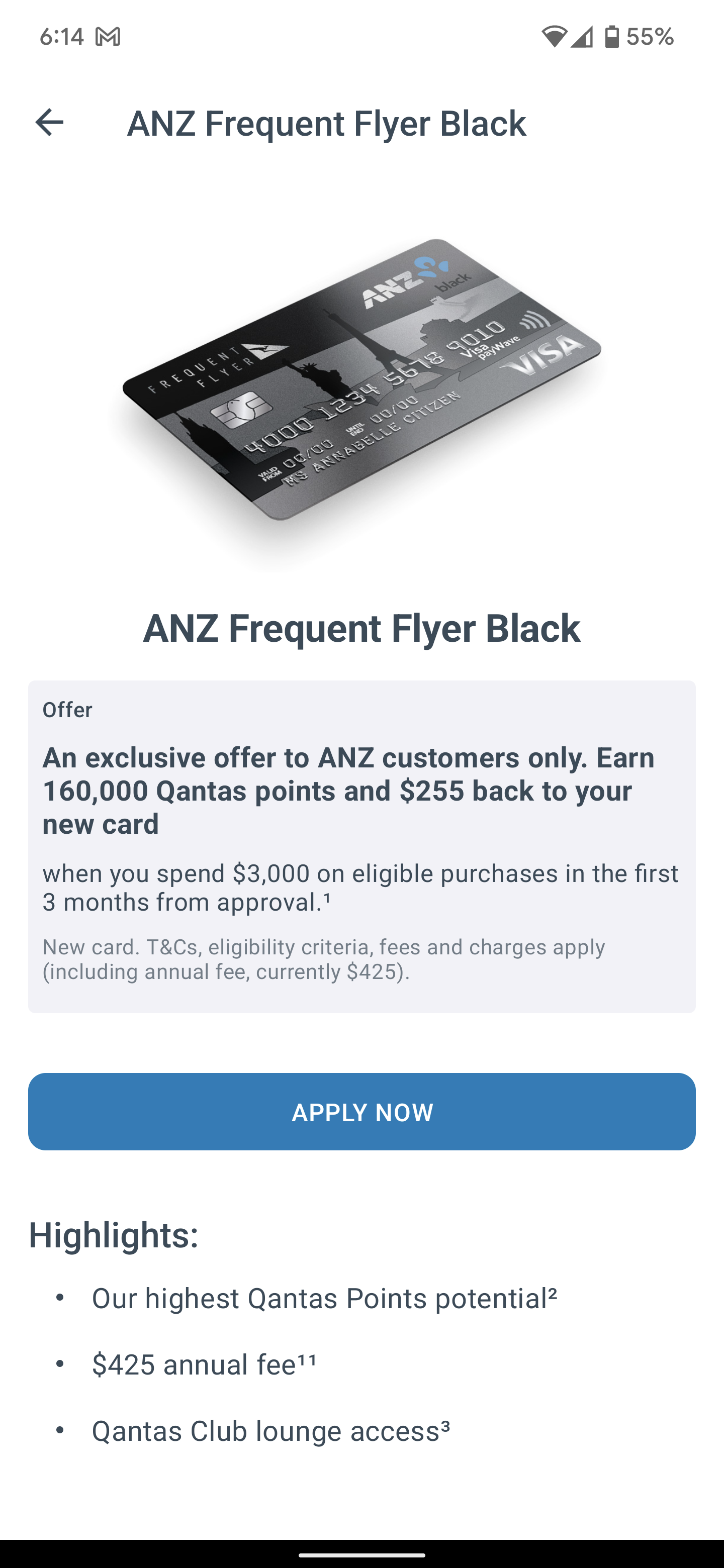

Found this huge Qantas Points offer in the ANZ app a couple of days ago:

An exclusive offer to ANZ customers only.

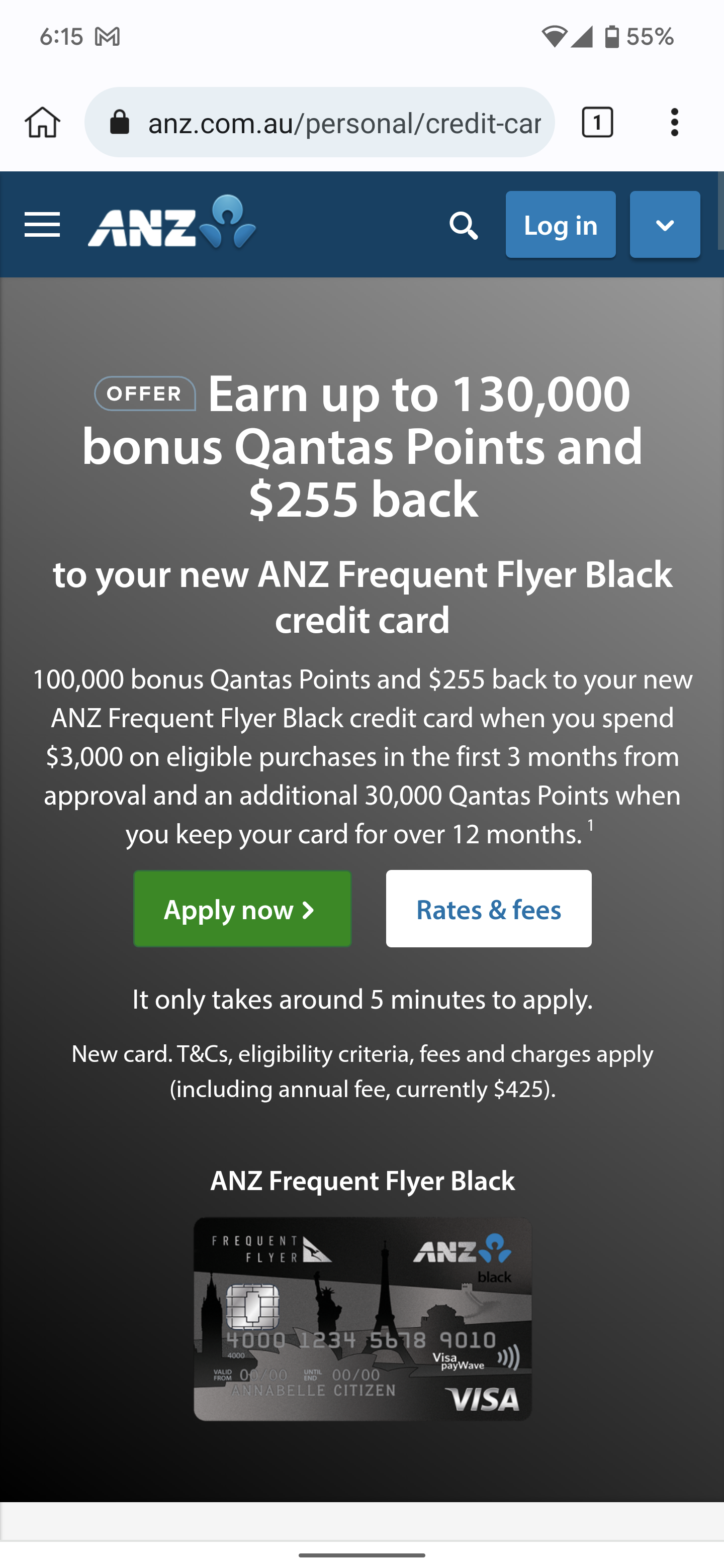

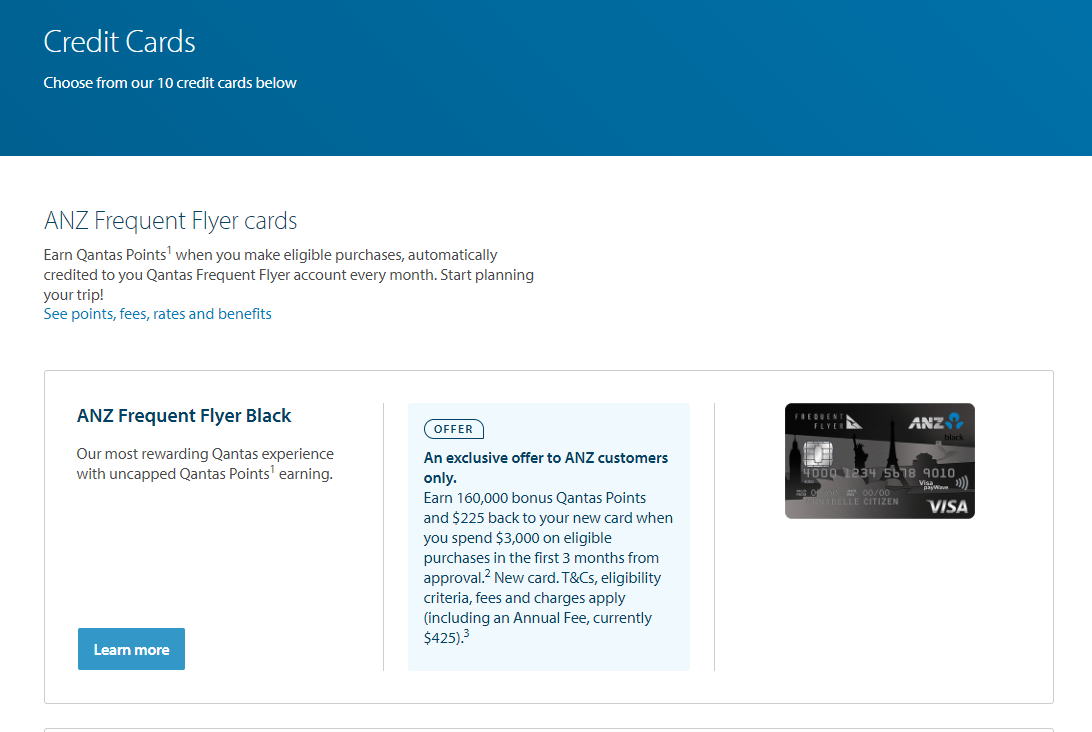

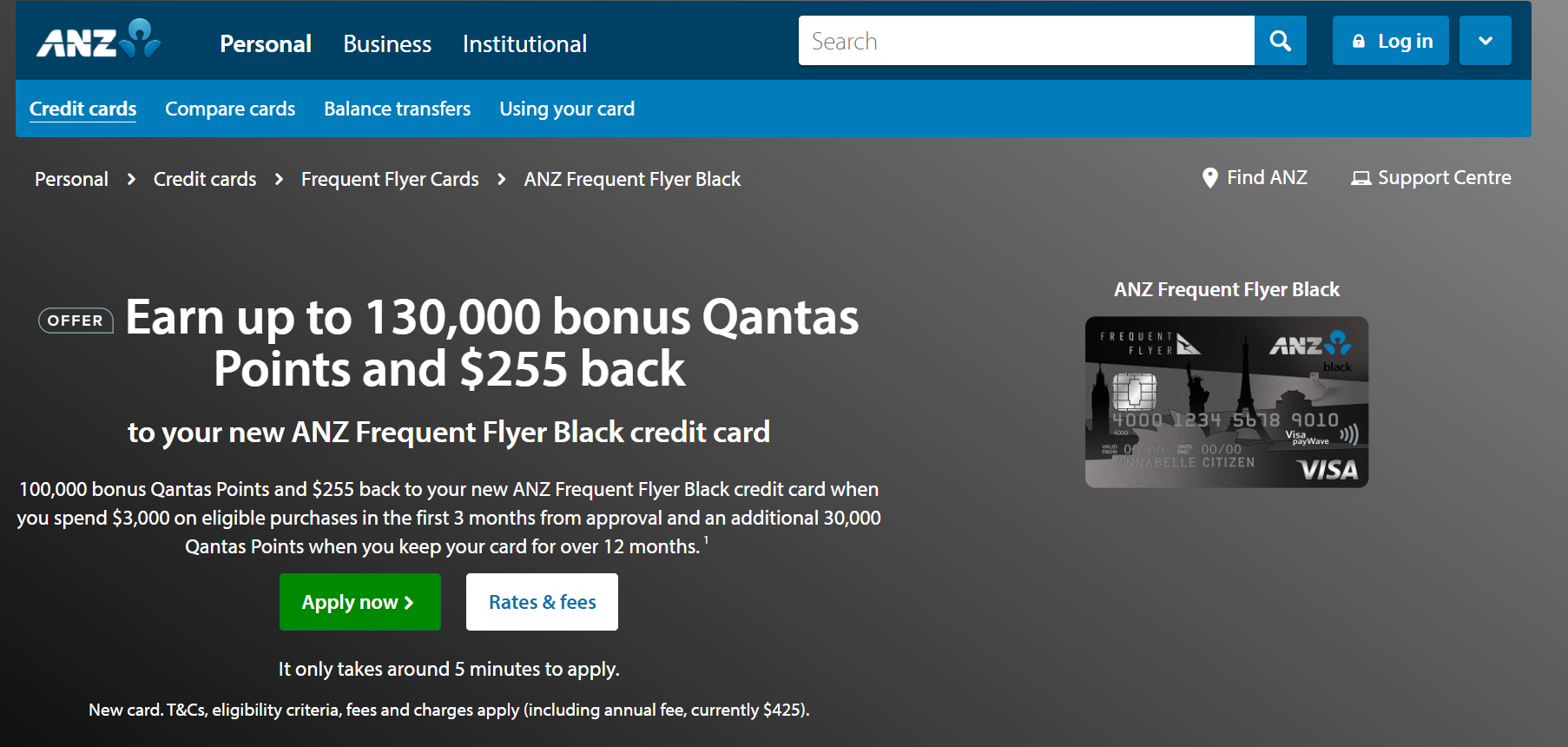

Earn 160,000 bonus Qantas Points and $225 back to your new card when you spend $3,000 on eligible purchases in the first 3 months from approval. New card. T&Cs, >eligibility criteria, fees and charges apply (including an Annual Fee, currently $425). Screenshot

You can get to this offer via ANZ Internet Banking in browser, or in the ANZ App.

If you aren't an ANZ customer: I mentioned this offer to a friend who then opened a transaction account and was able to immediately see the offer in their new internet banking and apply for the card. The basic ANZ transaction account is $5 a month, which you can get waived if you deposit $2k into the account each month (doesn't need to stay in the account). You could close the account once you get your bonus points (possibly once you get the card?)

Aside from this massive number of bonus points, card features are:

- Earn 1 Qantas Point per $1 spent on eligible purchases up to $7,500 per statement period

- A higher Qantas Points earn rate compared to all other ANZ Frequent Flyer cards

- Uncapped Qantas Points

- Complimentary Frequent Flyer Membership and a discount on a 1 year Qantas Club membership

- Two complimentary Qantas Club lounge invitations each year

- Complimentary insurances including International Travel Insurance

- Up to 55 days interest free on purchases

You can see the general details of the card (at it's usual lower offer value) here

I think this might be the highest consumer bonus points offer available at the moment, I certainly haven't seen any higher recently.

If you haven't earned Qantas Points from a credit card in the past 12 months, you may be able to stack with the New Cardholder Bonus of 20,000 points (from Qantas). The ANZ Black card is listed on the relevant page, and it doesn't specify that you have to click through the Qantas page to get the offer, but I haven't tried! The New Cardholder Bonus from Qantas ends on March 31 (there's no end date listed for the ANZ card offer).

Edit: Clarified end date in post applies to 20k top-up offer, not 160k sign-up offer.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Tempted but..

I’m not an ANZ customer.