Today, AMP has once again upped their term deposit rates over a range of timeframes, effective immediately. The last increase was only seven days ago.

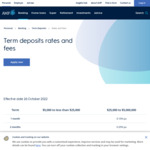

Highlights are for deposits over $25,000 up to $5 Million.

| Term | Interest rate |

|---|---|

| 1 year | 4.10% pa |

| 2 years | 4.55% pa |

| 3 years | 4.70% pa |

| 4 years | 4.85% pa |

| 5 years | 4.95% pa |

"No account-keeping fees apply to AMP Bank’s Term Deposits. Instead you will earn interest paid at terms you select or on maturity, depending on the term you choose for your term deposit. You may open as many term deposits as you like each with a different term or invested amount. You will receive your interest earnings at the end of the term or, if you would like to be paid more frequently, at a slightly lower rate on terms of one year or more. You can receive those earnings every month, every three months or every six months instead of annually."

UPDATE: AMP TERM DEPOSIT RATES HAVE BEEN REVIEWED AGAIN, EFFECTIVE 7 NOVEMBER 2022 - no changes to the rates above.

signal for another cash rate increase next week?