I'd rather buy an apartment near the CBD/my workplace, than buy a house 1.5 hours away in the middle of bumble(profanity). But apartments don't appreciate like land, therefore aren't good investments.

If I want to use the first home buyers scheme, I have to still live in the house for 1 year, which sounds stressful. Even assuming I complete my year of hell, and begin renting out my property, the rent most likely won't cover the mortgage. So for 30 years, I'd be pissing away like $200 per week. BUT the big advantage of a house, is that if you live in it for a few years you can sell it with NO capital gains.

Compared to shares, which incur a capital gains tax, when you sell them. Half off capital gains (if held for more than a year) is worse than no capitals gains. Plus shares are more diverse, house prices are pretty much determined by how desperate Indian immigrants are, and how rich Chinese immigrants are. If they decide "(profanity Australia", and move to an actual good country, my investment would be completely (profanity).

So, to maximize my wealth I'm forced to play into this (profanity) country's ponzi scheme. (Profanity) Australia.

Shareholders, how do you justify paying like 20 percent capital gains, when you sell?

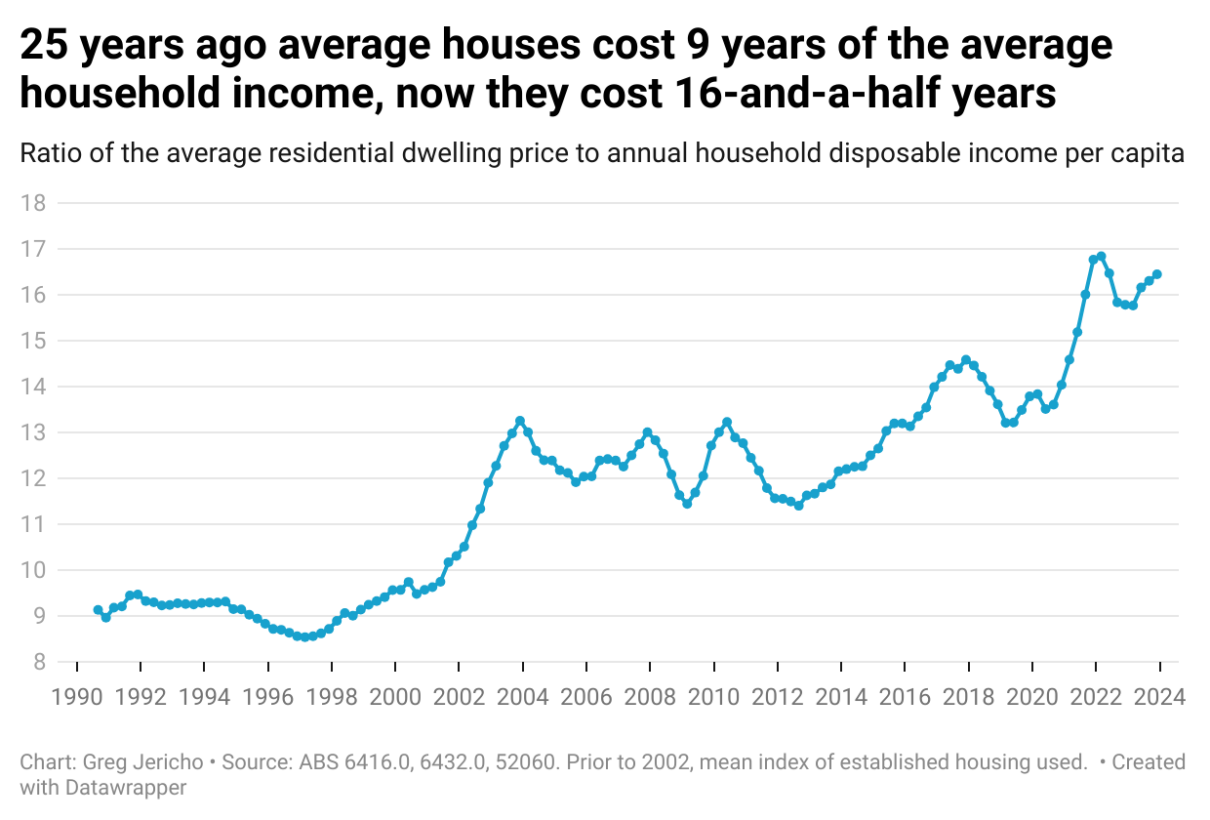

{kind=link}

neither singapore nor switzerland are remotely similiar to here. For one you need to visit switzerland, what you avoid in tax is more than made up for in cost of living. similarly singapore has great income tax, but it also doesn't have the cost of providing infrastructure, the total area of Singapore is less than 10% the size of Sydney and similarly the cost of living there is much higher than here.