From their website:

- Attractive returns: RateSetter offers attractive returns by connecting you with creditworthy borrowers

- Simple: simply select a term, amount, and rate you wish to earn

- Provision Fund protection: the Provision Fund can help protect you from borrower late payment or default

- A peer-to-peer pioneer: the RateSetter group is one of the largest peer-to-peer lenders in the world

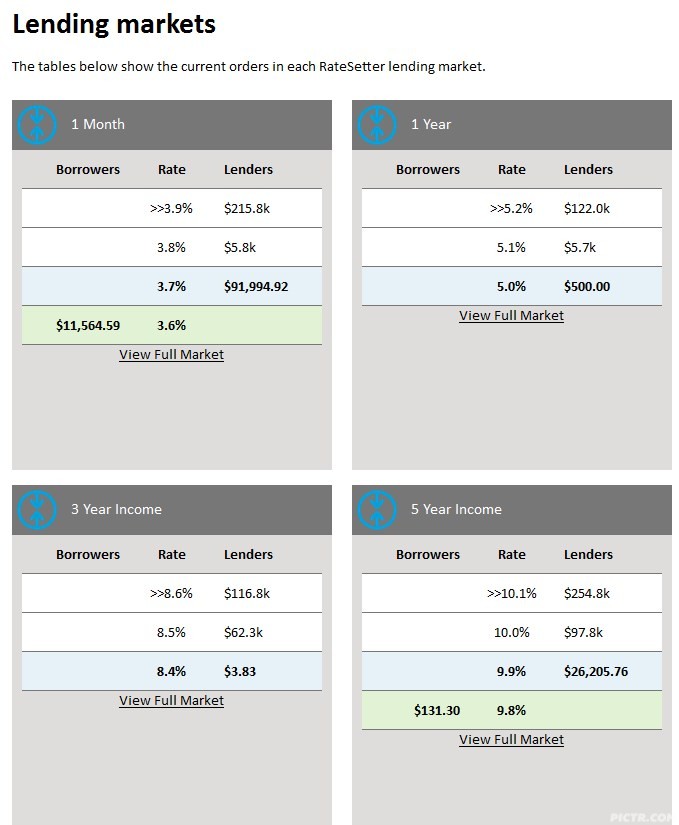

Current rates (Changes daily but usually not massively):

- 1 year @ 5.5% PA

- 3 year @ 8.5% PA

- 5 year @ 9.9% PA

Personal experience:

I have used Ratesetter for over 1 year now and have been pleased with the support and return. The provision fund (which is a form of protection, not to be confused with insurance) has held up rather well and this means that if someone were to default on some of my loans then I most likely wouldn't have a loss. It's best to spread your loans into smaller lots to mitigate risk. I've found that sometimes people pay their loans back early but you can easily lend the funds out again. Make sure your funds are either automatically withdrawn to your designated bank account or relent out otherwise you will miss out on interest if you have money sitting in the non-interest account. Each year Ratesetter automatically makes an annual tax summary so you don't have to worry about the complexities of having tiny amounts of money leant out at slightly different rates.

Ratesetter also publishes their loan book of borrowers which you can find here: http://static.ratesetter.com.au/loanbook/20160630LoanBook.xl…

You can deposit fairly easily via Bpay. It's worth doing some research on the risk and reading the PDS to make sure it's right for you.

For the first 1,000 referrals, with a maximum of 5 referrals per person

MOD: Please

- Do not add your referral link in the comments.

- Use the user-referral system to add your referral link to RateSetter. Click on the edit link in the grey Referral Links box below.

Warning: This is an investment with a company that is not an Authorised Deposit-taking Institution (ADI). The Australian Government guarantee does not apply in the event of the company going bust. Please consider whether it is appropriate for you.

{kind=link}

Give me $2000 and you might get $1000 interest after five years…. Or you might not….