Hey everyone!

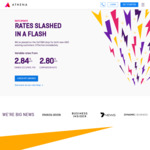

RBA announced a 0.25% drop in the cash rate today. For the third time in a row, we’ve passed on the full RBA drop for both new AND existing customers. Effective immediately.

Our latest rates are:

Owner Occupier, P&I: 2.84% variable (2.80% CR)

Owner Occupier, IO: 3.34% variable (2.99% CR)

Investor, P&I: 3.24% variable (3.20% CR)

Investor, IO: 3.34% variable (3.24% CR)

Our local Home Loan Experts are available to help out 7 days a week.

Features

No Athena fees: No application or valuation fees, no annual or monthly fees, no exit fees.

Automatic Rate-Match: New and existing customers will always get the same rate on a like-for-like loan.

Fee-free Redraw: Athena reduces the amount of your home loan balance by 100% of the amount in your Redraw.

Loyalty bonus: We’ll reward you with a 0.01% discount on your rate for each of the first 5 years just for making your repayments.

Are you guys looking into people who's self-employed yet?