Tic:Toc have a leading rate for their Fixed 1 Year P&I Investment Home Loan.

Loan features

- Minimum 10% deposit/Maximum 90% LVR (after LMI added)

- No upfront or ongoing fees

- Unlimited additional repayments

- Free online redraw

- Optional offset available for $10/month

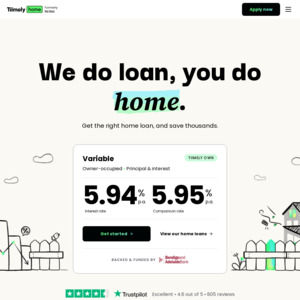

- Roll-to-rate of 2.84%p.a. after 1 year

- Up to 30 years loan term

- Fully online application

- Bank-backed and funded by Bendigo and Adelaide Bank

Eligibility

- Property type – must be buying or refinancing an established property (not off-the-plan or under construction)

- Location – property must be located in a capital city or major regional centre

- Borrowing amount – at least $50k but no more than $3m

- For loans under $2m, at least a 10% deposit or equity, plus savings to cover fees and charges such as stamp duty. If you have less than a 20% deposit, you'll need to pay Lenders' Mortgage Insurance (LMI). If you choose to have LMI added to your loan amount (instead of paying upfront), LVR must not be greater than 90% after LMI is added

- Employment – either PAYG, or self-employed for at least 2 years

- ID – passport, driver's licence, or Medicare card

- Country – open to Australian citizens or permanent residents who live in Australia

Offset account

Get an offset account with your home loan for $10/month. When you choose an offset account for our Variable P&I Investment Home Loan, the comparison rate will be 2.92% p.a.

Our 100% offset accounts are optional and available with all of our home loans (even fixed rate home loans). They fall under the ADI licence of Bendigo and Adelaide Bank and are covered by the Financial Claims Scheme. They also come with a nifty VISA debit card 💳 You can find more detail here.

Legal things about our rates

No honeymoon rates

Existing borrowers may have a different interest rate, depending on the price we were able to negotiate with our funder at the time the loan settled, and any reductions made over time. We don’t do honeymoon rates, or make loyal customers subsidise lower prices for new customers. We’re transparent with our rate history, you can read about it here.

Our current rates

Our rates are current as of 8 July 2021; available to all home loans approved on or after this date, and they can change. Our comparison rates are calculated for a $150,000 loan over 25 years. They factor in our fees associated with applying for the loan; our ongoing fees and our fees associated with leaving the loan. Our fixed loans roll to a variable principal and interest rate at the end of the fixed term. If the interest only period is not specified, the comparison rate is calculated on a one year period.

WARNING: The comparison rates are true only for the examples given and may not include all fees and charges. Different terms, fees or other loan amounts might result in a different comparison rate.

Tic:Toc Home Loans. Australian credit licence 496431. ABN 41 605 696 544.

2.14% is quite high, higher than big 4.