Hi XXX,

You're being dropped. Again.

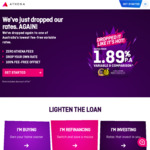

Today we’re dropping our rates to a new record low 🔥 This means your rate will be automatically dropped today. We’ll be making this change during the day, and your interest calculation for today will be on your new rate. We’ll send you confirmation of this new rate for you to see in Home Hub tomorrow, but in the meantime, we wanted you to be the first to know.

___________

Also don't forget now they offer fee free offset account also, see my below updated post about that and clarification reply from Athena about offset account.

https://www.ozbargain.com.au/node/673396

| Owner Occupier P&I | Interest rate | Comparison rate | Loan to value ratio |

|---|---|---|---|

| CelebRate | 1.89% | 1.89% CR | 60% LVR |

| EvapoRate | 1.94% | 1.91% CR | 70%-60% LVR |

| LibeRate | 1.99% | 1.93% CR | 80%-70% LVR |

How did they calculate the V in LVR? Was it close to current market value?