Hi XXX,

You're being dropped. Again.

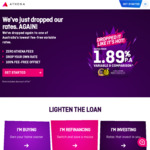

Today we’re dropping our rates to a new record low 🔥 This means your rate will be automatically dropped today. We’ll be making this change during the day, and your interest calculation for today will be on your new rate. We’ll send you confirmation of this new rate for you to see in Home Hub tomorrow, but in the meantime, we wanted you to be the first to know.

___________

Also don't forget now they offer fee free offset account also, see my below updated post about that and clarification reply from Athena about offset account.

https://www.ozbargain.com.au/node/673396

| Owner Occupier P&I | Interest rate | Comparison rate | Loan to value ratio |

|---|---|---|---|

| CelebRate | 1.89% | 1.89% CR | 60% LVR |

| EvapoRate | 1.94% | 1.91% CR | 70%-60% LVR |

| LibeRate | 1.99% | 1.93% CR | 80%-70% LVR |

Not sure how strict they are, but going through their application process was like wading through treacle.

Repeating the same information with multiple assessors, uploading and reuploading the same pay slips and other financial information and enduring repeated assurances that approval is imminent, just waiting for another assessor to verify the application. My income is over $300k in a long term job, 60% LVR and outright owner of another residence - but I still couldn't get an answer off them inside 5 weeks before giving up, chiefly due to knowing I wouldn't have the patience to deal with that level of responsiveness over a twenty year loan…