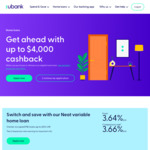

Ubank from today offering up to $4,000 cashback for refinances OR purchases.

$250,000 - $999,000 = $3,000

$1,000,000 and over = $4,000

Fully digital process, currently 1 business day turnaround (likely to increase with this deal)

Be prepared to securely use your online banking credentials - UBank utilises open banking and will 'scrape' your transactions, so just giving you the head's up here.

Here's the rates

Owner occupier, variable, P&I (no offset, however free and unlimited redraw)

LVR up to 60% - 4.14% (comp. 4.16%)

LVR up to 70% - 4.19% (comp. 4.21%)

LVR up to 80% - 4.24% (comp 4.26%)

LVR up to 85% - 4.94% (comp 4.96% and no LMI)

Investor, variable, P&I (no offset, however free and unlimited redraw)

LVR up to 60% - 4.39% (comp. 4.41%)

LVR up to 70% - 4.44% (comp. 4.46%)

LVR up to 80% - 4.59% (comp. 4.61%)

The terms

We want to help your customers get ahead with money, which is why we'll give them up to $4k cashback when they take out a new home loan with us or bring their existing home loan across to us!

From 12 September 2022, your customers can enjoy cashback when they purchase or refinance on an eligible 'Neat' or 'Own' ubank home loan and have an LVR of 80% or less.

How it works:

• $3k cashback for loans between $250,000 and under $1m

• $4k cashback for loans of $1m or more

• Apply between 12 September 2022 - 30 November 2022 and settle by 31 January 2023

• Not available for refinances within NAB Group

Whether your customers are wanting to get their first home loan, or second, or even just refinancing, there's no better time than now.

Already have a customer with a pre-approval or unconditional approval with us in the pipeline? As a gesture, we may offer the cashback to already approved customers, provided all other Ts&Cs and criteria are met.

COMPARISON RATE WARNING

Each comparison rate is based on $150,000 over 25 years. These comparison rates apply only to the example or examples given. Different amounts and terms will result in different comparison rates. Costs such as redraw fees or early repayment fees, and cost savings such as fee waivers, are not included in the comparison rate but may influence the cost of the loan. Comparison rates for Interest Only Fixed Rate home loans are based on an initial Interest Only period equal in length to the fixed rate period. Comparison rates for Interest Only Variable home loans are based on an initial 5 year Interest Only period.

Hope you find this useful,

Aidan

Owner & Mortgage Broker at Blue Owl Finance

aidan@blueowlfinance.com.au

www.blueowlfinance.com.au

Link to my calendar to book 15 minute appointment here https://www.blueowlfinance.com.au/book-online

Note - I do not offer broker cashback, some brokers on OzB do offer their own cashbacks.

ABN 27 646 433 374 | Certified MFAA Member 230928 | Australian Credit Licence number 387025 | Credit Representative’s number 527699

Not available for refinances within NAB Group - Well that's that :(