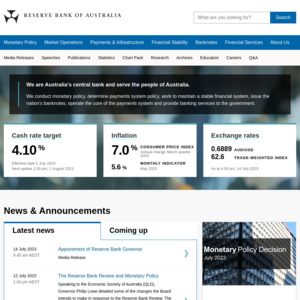

Lowest for ~2 years.

The RBA's official cash rate was last below 4 per cent in May 2023, before it was raised to 4.1 per cent at the June 2023 meeting.

Yay for borrowers, nay for savers.

Lowest for ~2 years.

The RBA's official cash rate was last below 4 per cent in May 2023, before it was raised to 4.1 per cent at the June 2023 meeting.

Yay for borrowers, nay for savers.

markets aren't spiking up like they did last time.

Cut was priced in weeks ago

The Canary will be the price of gold, if it goes up the world economy is in the lurch.

Sure, but the gold mining industry will go ballistic. Australia does a lot of gold mining.

Strangely though the share price of miners isnt that closely tied to the commodity

I learnt the hard way

@Drakesy: Did the major shareholders who are also on the board of directors keep issuing shares to themselves diluting every one else's positions and uncoupling the share price from the gold price?

@tenpercent: I mean thats expected. But yeah strangely the share price of many miners don't directly follow the gold price.

Bit weird.

AMP already sent an email out that they are cutting their standard rate by .25% from Friday the 23rd May. Their max Saver rate will be 4.70% if conditions are met, otherwise .50%.

Here we go again. All the others will follow…

“Inflation continues to moderate”… meh. This rate cut is inflation related and we will like see further cuts as govt spending goes nuts.

All the freebies being given away will have to be paid back in one way or another.

Economy is on the ropes and they go and prop up the housing market even more.

Huzzah!

The housing market is our economy.

Apologies my bad.

Yes - sad reality

Overpriced housing and digging up rocks - Australian economy in a nutshell

Exporting water, is what we do.. We waste trillions of litres of finite water de-dusting haul roads and washing rocks,suppressing dust.If the water was priced at a tiny % of the basic commercial quantity/quality rates, that industry pays elsewhere,we are pissing millions of $$ a year in a precious resource, against Twiggy and Ginas bank vault walls.

Interest rate drop means more borrowing power and higher house prices.

Kicking the can down the road….

Damned if they do, damned if they don't.

Whatever they do, someone is always going to bitch and moan.

It is what it is.

Damn, wish they had gone with the 50 points reduction.

Everything that is relevant is up double digit %’s year on year.

They don’t know what inflation is or how to calculate it, so I’ll never be confident in any monetary decision.

St George posted a savings update link on Facebook (not accessible from anywhere else) = .25% savings rate decrease from 30th May

https://www.stgeorge.com.au/personal/bank-accounts/savings-a…

Unibank (Teachers Mutual & all affiliates) also reducing loan & savings rates by .25% from June 1st (that will also apply to no longer on offer products like the Hiver Saver)

https://www.unibank.com.au/about/member-news/2025/unibank-an…

Other than these 2 and AMP reducing by .25% from Friday (via email advice), other banks have not made any official announcements yet.

Some banks, like Rabobank, based on past practice are expected to apply a decrease and notify via email after the fact.

I do not recommend moving money around as all banks will eventually apply the rate decrease to savings accounts within days of each other.

Do you reckon uBank will reduce the current 5.10% ?

And also, is it safe to park around 100k in uBank? Hearing some very mixed reviews about it. As of now it is the only bank with no grow requirement, giving a high interest rate.

Why would it not be safe? They are still an Australia bank, and subjected to all australia laws. They are backed by NAB and an ADI (part of goverment guarantee scheme)

Didn't get the email? 4.85%

Bad time coming for cashparks.

The green light for more bank gouging.

$2,000 pre tax saving p.a. for me

Better than the 4.25% p.a. increase from 2022

This cut was mistake at a time when yields are going up all over the world.

After checking a few other bank web sites, the following banks have also dropped rates without any notice

Great Southern Bank dropped all saving rates by .25% - Home Saver now 4.75%, Future/Advantage Saver now 4.35% (effective immediately)

Macquarie Bank dropped their saver rate from 4.75% to 4.5% and CMA Accelerator from 4.4% to 4.15% effective from Friday 23rd May

No action yet from ING, Ubank, BOQ, ME Bank, Rabobank (but expected to follow soon)

i expect BOQ will drop rate without any formal announcement comms to holders

UBank , Rabobank have dropped.

Rabobank by 0.30%. How do they justify that?

Justified in the name of more profit for the bank - when rates go up they either skip or partially increase, when they go down they go down more than the RBA - that is the Rabobank way. Previous drop was from 5.45% to 5.10% ( -.35%) now 4.80% (-.30%).

Rabobank HISA Decreased to 5.15%, Premium Saver 4.8%!

And too late to withdraw money today… Have to wait until monday

it's not to late - transfers will take place with next BECS schedule (several left today) - however why move - they have all dropped & only ING remains higher & most of us already maxed that to $100K

You may be right, but the last time I tried to send money out on a Friday early afternoon (to St George) not only did it not arrive until Monday, Rabo deducted it immediately so it didn't earn any interest over the weekend. I don't want to risk it

Just received from 27/5/25 Ubank earn up to 4.85% for $0-$100K

4.40% for total balances between $100K -$250K

Sick joke

YAAAAY … now lend me some $ so I can default on that loan also!

genuinely curious, who are the people most upset about falling deposit rates? I've always thought of it as nothing more than a short term park of funds. Once you get taxed on your 4-5% p/a in a HISA you are literally losing money as it's less than inflation?

Retirees or just unemployed people with paid off mortgages and have some spare cash?

They won't be taxed that much on their interest from their savings.

Can’t feel too bad about people with fully paid off mortgages. Although their assets are relatively illiquid

some people only rely on their savings income - so most of it is tax free or taxed at 15% - if retired and on a pension then it is 100% tax free

Tax free unless your interest is over the tax free threshold.

or retired drawing from an SMSF pension account - there is no such thing as a tax threshold for your super money with only requirement to draw a minimum % amount to live on that is age based. Statisticaly there are more savers than "loaners" in Australia - more people depending on their savings - so when the RBA drops rates there are more loosers as a result - statistical facts never make headlines - people owning money, a good % of which will never repay in their lifetime as they borrowed well beyond their means, always make a loud noise & influence the politics of decision making.

St George is a very special case & rate is lower than Rabobank already from 30th May (not worth moving for just one week) - St George processes received funds overnight. I have Rabobank linked to Unibank (ex Hiver Saver) as it is a good place to park large amounts of money without max limits and onerous conditions - I just move the money between 2 savers on 1st of each month (instant transfer no matter what the day is unlike St George) and take out what I need via OSKO instantly on the same day. Money arrives on the next BECS schedule once initiated from Rabobank, if done early morning it always arrives between 11:45am and noon.

Defence Bank Isaver dropped to 4.65% today

ME down to 4.85%, only 0.15% drop

Yes, only .15%, however the standard rate is reduced by .50% to just .05% (why not zero ? ) so savers are penalised even more if they miss a hoop (like forgetting to deposit $2K the previous month).

This proves that banks are accountable to nobody and that any recent investigations on the subject have produced zero outcomes or improvements.

Governments and regulatory bodies make a fuss and then do absolutely nothing. As a result bad banks keep behaving badly.

From 30 May 2025, the following rates will change on your HomeMe Account:

The variable base rate will be decreased from 0.55% p.a. to 0.05% p.a.;

The variable Bonus Interest Rate for balances up to $100,000 will be increased from 4.45% p.a. to 4.80% p.a

add that to the MEB .55% drop in March - so a total of .70% drop vs the RBA .50% rate drop

Might as well mention that ING drops from 5.40% to 5% from Monday 2nd June. Drop is .40% + .10% in March so the full RBA drop in the past 2 meets.

Bad times for savers are returning in a fast and furious pace.

Like ME Bank, the standard rate is only .05% if bonus criteria is missed (everyone is going Dutch = Stingy)

Effective ING Savings Maximiser Rate from 02/06/2025

5.00% p.a. highest variable rate (decreased from 5.40% p.a.), made up of:

4.95% p.a. additional variable rate for eligible customers (decreased from 5.35% p.a.)

0.05% p.a. standard variable rate (remains unchanged)

Virgin Savings also posted the folowing on their Web SIte

We’re changing the interest rates on our Boost Saver.

Effective 2 July 2025, your new Boost Saver interest rate will be up to 4.45% p.a. when you continue to meet the Monthly Criteria.

And, if you also enable the new Lock Saver Feature, your interest rate will increase up to 4.75% p.a.

BOQ Smart Saver now 4.75%, Future Saver 5.10%

Yikes.

So for anyone over the age of 35, there is zero incentive to go with BoQ over ubank.

Mobile only account access, a lower interest rate, double the monthly deposit requirement and 5 transactions per month.

Something tells me they don't want anyone aged 35+ and only want gullible young people.

The account has no real increase requirement & it can hold savings up to $250K - that is the advantage over other accounts. The criteria is easy to meet as a 5 X card transaction & a $1K instant transfer between BOQ and ME Bank. I actualy do $2K from ME Bank to BOQ and back to ME Bank to satisfy the ME Bank criteria. I keep the bonus rate activated, even though I have no money in BOQ, just in case I need to move money out from another account and this is the only available account to do so.

You're happy with a 4.75% account that requires you to deposit $1k and 5 card transactions per month, as opposed to ubank offering 4.85% for a $500 deposit?

@scalebearer: It is an option depending how much savings you have. Ubanks drops to 4.40% for amounts over $100K. I use Ubank (4.85%), ING (5%), ME Bank (4.85%), Rabobank (4.8%) and will use BOQ at 4.75% if necessary or anything else that may be better in the future.

Fully expected (with no prior advice) and the reason why even thought enticing while it was stil 4.90%, I did not move any money back to BOQ.

Obviously we all know that the RBA did not cut interest rates in July, that did not stop UBANK from doing a .25% rate drop today (email send out today), the only thing made easy is the decision to no longer use UBANK -:) the balance increase requirement stays but reduces to $1 from October but that does not really help savers that also need to spend

| Email from UBANK |

|---|

| From today, you can earn up to 4.60% p.a. bonus interest across your combined savings between $0 - $1 million. |

| From 1 October 2025, you'll need to grow your combined balance across all your Save accounts (excluding linked offsets) by $1 each month |

The US cap gone to 60t. Uber ahead of cba. MAGA!