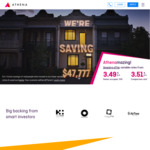

Cracking launch rate from brand new home loan provider, Athena - provided you can meet the 80% LVR requirement.

Offer is for refinances only.

No fees (Except for Third Party Fees) and no redraw fees

Perhaps the biggest draw card is the claim for the like-for-like auto rate match which i read as a promise of no back book pricing, so you are on the same rate as new customers for the same class home loan. Other low margin lenders like Ubank (And generally all other lenders) will creep the rate up on their back book after they hook you in on a good new-customer rate.

Other rates appear exceptional as well:

Owner Occupied Principal & Interest: 3.49%/3.51%

Owner Occupied Interest Only: 3.99%/3.70%

Investor P&I:3.89%/3.91%

Investor Interest Only: 3.99%/3.95%

An ADI with offset balance guaranteed?