RBA slashed the cash rate to 1%

Checked Athena home loans and they swiftly slashed their loans!

Very good deal, and good reviews online

RBA slashed the cash rate to 1%

Checked Athena home loans and they swiftly slashed their loans!

Very good deal, and good reviews online

$250 credit each for referee and referrer.

Has anyone had any luck with refinancing with these guys for small properties? We're talking 40-55SQM 1 bedroom apartments/units within 10km of Melbourne CBD?

Would love to move the whole lot over to these guys.. but have had bad experiences in the past with other lenders & small places.. (specifically reduce loans cough cough).

I don't like your chances. With an 80sqm two bedroom unit in the city they do want 70% LVR, didn't see other requirements and it may be more relaxed further out.

Going through with tic-toc at the moment and they want at least 60sqm in the CBD.

Alright this is good info. Ill assume 70% LVR.

Cheers!

boq is doing 2.99 fixed for 3 years. u bank - 2.99 for 1 year fix.

It is likely there will be another rate cut before the end of the year, and you might lose the benefit of the lower rate quickly. Also no offset, or ability to make large additional repayments or refinance (without break cost) for fixed rates. Those are good fixed rates, but fixed rates are not for everyone.

Do you know good variable rate to refinance 600K+ ip home loan at the moment? with banks & non-bank lenders.

what is "ip home loan" do you mean P&I (principal and interest)?

In order to answer any question on rate - need to know at a minimum the following:

@SydneyMoney: LVR < 80%

Investment property

Principal & Interest

PAYG + rent income via bank statement (rent > monthly p&i loan payment)

Currently home loan is with NAB

Prefer refinance with bank with offset account. Have 50K in offset account.

I want to know best interest rate (in best scenario) before discussing in details. Thank you.

@kctt: Athena are good - I have my two investment properties with them now.

Why do you have an offset account on your investment property? Have you had advice from an accountant or financial consultant?

Advice I've had is that as soon as you lower your loan on an investment property you cannot (legally) raise the amount you are claiming interest on.

If you have a home loan, you are much better off with the offset against there (and maximising the investment loan).

@tallmantim: @kctt not sure why you have pi with your IP other than the interest rates as having offset is basically useless as you cant really debt recycle.

@tallmantim: sorry I've got confused as I previously read the opposite "general" advise from other comment here;

https://www.ozbargain.com.au/node/461302#comment-7351596

Does your comment compliment that? Care to explain a bit more please. Newbie here

@tallmantim: Just for your information, offset is the only way you can 'reduce' a loan and increase it back to its initial amount.

This is because the loan itself has not been adjusted and thus you have not impacted the nexus for deductibility purposes.

Tax agent :P

@tallmantim: Already paid off my home. Don't have intention to flip ip anytime soon so I'm happy to pay p&i for better interest rate.

@tallmantim: That's exactly why you want an offset on an investment (or even potential investment) loan. Any extra money you have you can put against the offset instead of the loan. Obviously if you have other non-deductible debt you're better off paying that down first, but plenty of investors have already paid off their residence (or maybe don't have one and later want to take the money back form an investment offset to buy one). A lot of people are wary of taking on multiple investment loans in addition to one on their home.

Personally I've paid off my extremely modest home, and am looking towards and investment loan for the next 5-10 years, before I'll take money out of the offset from the investment loan to upgrade my home. Thus I want an investment loan with as low of a rate as possible and an offset (ideally interest only, but at the cost of a much higher interest rate it may not be worth it).

So basically I can't use a redraw on an investment loan since I'll want that money back and want to keep the investment with as much deductible as possible, and I don't have a home loan to offset.

Also note that they charge a $10 monthly account keeping fee

if you're deciding between 2.99% and 3.1%

the $10 monthly fee should be accounted for in your calculations for interest savings

Genuine question - in reality what are the odds that interest rate goes below 3% in next 3 years.

(current rate 1% and banks asking 3.3-3.7% for variable loans)

BOQ offered $1000 cash back to me.

CBA forecasted in their books official rate to hit 0.75%

so if we get another drop then you'll see Athena under 2.99% if they follow their trend

Athena didn't exist six months ago so only time will tell as to whether they increase rates independent from the RBA. My suspicion is they will, they need to profit somehow and playing a cost-differentiator strategy can only last so long.

Very true.

Although the lack of fees to withdraw and move on makes that less of a risk. If they jack the rates then you can move on to elsewhere without loss.

If i had my home loan with Athena and they go broke, do i get my house for free?

no, someone will buy their books and increase rates

@[Deactivated]: Nope, people will always pick up a toxic loan, even if it was onsold for 1c in the dollar.

@serpserpserp: So technically, yes its possible.

Especially after the GFC & banking royal commission.

So technically, yes its possible. Especially after the GFC & banking royal commission.

No. I mean another FI will pick up the loan from Athena (if they went under) for your home loan. The borrower is never let off the hook. Athena will only make 1c out of my proposal above, the new FI will make all the money and take the risk on your loan.

Sorry I used toxic in the wrong context here. But what you should know is this. You will never get a free house from a lender going under.

I believe they might be one of the only lenders in Australia that don't do separate pricing for their backbook, so you should always be on the new customer rate for your loan type. They can't really increase their new customer rate too much or they won't be competitive for new loans so you should in theory always be on a decent rate with them.

I believe they might be one of the only lenders in Australia that don't do separate pricing for their backbook.

How can you possibly know this for certain?

so you should in theory always be on a decent rate with them.

Because you "believe" they don't reprice their backbook (remember they have only been around 6 months too), doesn't mean this theory is sound.

Athena do advertise that new borrowers will never get better rates than existing borrowers - and that they don't use honeymoon rates. Whilst this is no guarantee they would surely end up with some egg on their face if they backflipped.

I can't guarantee it, but they seem to. This is their whole differentiating premise about their product and their brand identity on their website so its not likely they are going to backflip on it anytime soon.

ACCC will have a ball if they start repricing the backbook after they made a big promise not too.

@[Deactivated]: Hey Babadook, you're right we don't have a backbook. Every existing customer gets the same rate that new customers get for an Athena like-for-like loan. This is an Australian first and we think it's only fair.

You are wrong here. They have the ability to raise capital as a private company. They do not have to manage depositors rate and only deal in home loans where all the money is. In saying that they couldn't care less about the community and I would love to know their CSR credential. Customer owned banks all the way for me….. Athena talk a big game but it is all marketing and not much else

Thanks, bought 2 houses. Just in time for Christmas :)

Twenty more carrots to go. Lol.

Great stocking fillers

When you refinance with these guys, do they cover all the exit costs from your old lender (title signover, exit fees, etc)?

Ask them and let us know

highly unlikely they will cover fees that your existing provider charged and also highly unlikely they will cover the mortgage registration fees. They just advertise no application, valuation, ongoing, or settlement fees. UBank also don't charge these fees.

I figured that was the case. Makes refinancing a pretty poor option for lower value loans - after accounting for all the transfer costs you're not getting much benefit from a slightly lower rate.

no I would say if your home loan is <$100,000 it's probably not worth refinancing owing to the costs. Unless you happen to be on a 5%+ loan rate or something rediculous.

besides exit fee, is the only other fee the mortgage registration fee? this ridiculous how many fees there are and worst of all banks dont even state it clear. read it in cba's discharge document and they dont mention mortgage registration ever. they should just bundle all the fees together instead of having this confusing mess made to scam people who dont spend 20 hours reading their policy. even when i added all fees of big 4 by a 150k loan, it still is less than their actual comparison rate. literally the same as word trap contracts.

They paid a bonus last time when I checked with them which was enough to cover for the exit fees not sure if it still exists.

Do you know if this was a limited time thing or something? If they had a bonus $500 to $1k bonus to refinance with them I would refinance them in a heart beat. The only thing really stopping me is the high state/bank fees and unsure what the market will be like after another rate cut.

It doesn't mention on their website anymore…so I guess it's no longer available but it's worth to send them an email to confirm.

It was like $500 bonus per loan and I've done calculation and it's worth to switch to them.

Also curious to know how a refinance works as to what happens if they don't think the house is worth enough to cover the loan, or the loan isn't serviceable for some reason - even though the loan was approved by another lender previously. At what stage is your current lender 'told' about the switch or potential switch

Your current lender is only told when you sign a "discharge statement", which generally only happens after you are approved.

It looks like you don't have card or ATM access - so will need a separate transaction account like Macquarie or ING. The best thing about this offer? Gives me the opportunity to have a serious chat with our existing lender…

They'll seriously won't care and will give you a token discount unless your a HNW account to them.

Know that the big 4 banks might give you a discount but are always making good margin from you.

It's worked before :)

Just had a chat with my lender. They've added another 0.22% to the discount. Very competitive now with the cheepies, and full banking to boot.

Damn. I wished that we didn't fix so much of our home loan. Our fixed investment runs out in 1.5 years and our home loan at the end of the year.

With Suncorp. Would charge a shitton to break the fixed loan.

In long term. VR always beat FR

Yeah but at that stage it was 4.49 v 3.99 so…

Not necessarily true (although it has been for the last 11 years).

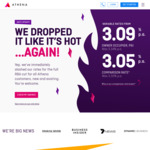

Reduce home loans variable rates are 2.89% down from 3.09%.

Been with Reduce for 2.5 years. Had one out of cycle increase and they delayed the last cut by 2 months (takes effect late July for existing customers)

Personally think the likes of Athena and Tic Toc look appealing

How much was the out of cycle increase? Scums!

0.15% (from memory)

Be careful around “offset” facility.

Care to elaborate. Are you referring to the fact they offer a redraw facility instead of offset.

think he is stating that these smaller brokers give you an offset account but with higher rates and some fees

this loan is for no frills home loan only

Redraw and offset are not the same product. They may work in similar ways but may have different tax implications down the line. Suggest doing some research to understand the difference.

For investment properties. Yes.

@serpserpserp: We’re not a bank

And never will be. That means we’re not covered by the government’s financial claims scheme, which guarantees “traditional” offset accounts up to $250,000 if bank lenders fail.

But don’t worry. If something was to happen to Athena (very unlikely!) we have contracts in place where a back-up servicer can honor your loan and agreements you have with us. That should include your Redraw facility. Your other option would be reduce the balance of your loan by making a lump sum payment into your loan using your redraw funds. That way you pay down your debt sooner and this can reduce your repayments if you want.

We’re not a bank

And never will be. That means we’re not covered by the government’s financial claims scheme, which guarantees “traditional” offset accounts up to $250,000 if bank lenders fail.

But don’t worry. If something was to happen to Athena (very unlikely!) we have contracts in place where a back-up servicer can honor your loan and agreements you have with us. That should include your Redraw facility. Your other option would be reduce the balance of your loan by making a lump sum payment into your loan using your redraw funds. That way you pay down your debt sooner and this can reduce your repayments if you want.

I received my "unconditional approval" from Athena last week and the contract documents arrived yesterday. Process took over 2 weeks which I was not overly impressed with and their contract seems incredibly one-sided (even by mortgage lender standards which seem to be inherently heavily weighted in favour of the lender). I've asked my solicitor to review before I sign on the dotted line but this immediate rate drop makes it even more attractive… Decisions decisions!

What are some examples of 'one sided' clauses within the contract?

Are they not all mostly same and sided towards lenders?

They could well be - it's been a while since I last went through this process. I'm not going to copy and paste specific clauses as I don't think it's the right thing to do (or even allowed). No doubt my solicitor will be able to confirm whether this is just "layman's bias" (which is indeed possible) or not. If I'm wrong I'm more than happy to comment again to that effect.

Thats the whole point, the contract is never to protect you.

Reduce has a (deserved or not, I don't know) reputation for great advertised rates, but a) increases out of cycle and b) not passing on cuts to existing customers. I'm looking at Tic-Toc in spite of slightly worse rates because I'm more confident in them over longer terms.

How is it possible that the comparison rate is lower than the advertised rate? Do they refund you a certain amount reach year for staying with them?

You get a small % off the standard rate each year you’re with them

A cheats way to make a CR lower than the advertised rate. They are most likely to jack the variable rate a few times over the course over the first year like a lot of these operators do. What they show you is just an informal honeymoon rate which unfortunately you don't know when it will end.

From Athena's website: 'new customers will ever get a better rate than existing customers' and 'We will never raise rates unnecessarily. Or sneak up a ‘honeymoon rate’'

I am not associated with Athena however I am in the process of an application with them. I checked these points in advance.

Yes

Quick question OP - current loan balance 200k and 300k in redraw ( total Balance 500k) does Athena Charge P & I repayments on 500k ( original loan balance) or on 200k ( Actual loan balance) and increase P & I repayments if and when I withdraw money from redraw? I understand that interest is always charged on the current loan balance but more keen on knowing how you charge P & I repayments as a whole?

All providers charge interest in the same way for the same type of account.

i am not sure - best send them a message

Offset please!!! I will refinance immediately when this happens!

Have asked, apparently that would require a deposit taking license and isn’t going to happen any time soon.

Do they have free unlimited redraws and allow extra repayments at any time (also free)?

Yes

Unfortunate, but good to know what's holding them back.

I gather you have tax deductible interest. For the average home/mortgage the redraw facility that Athena offer is fine.

@clio: I massively regret being an average home/mortgage customer. I bought a place 10 years ago and didn't elect the offset (why would I, I thought, it was a very slightly higher rate and had an annual fee). 10 years later my place would be perfect for the rental market, it would be bad to sell right now, but I can't really move without selling as I can't deduct the mortgage costs if I rent it out. Basically feel trapped in my home.

Hey it was 3.30 CR this afternoon I checked, now it's 3.05 lol, that's quick. My sis told me even though the smaller ones' rates are cheaper but they're not good at their service. Like a lot of people switching to the big banks for the service. So is that true?

I just had a chat with a broker, that's exactly what he said, literally banks without branches don't really have good services

Brokers have their own motivations - lenders that don't pay commission don't pay brokers.

exactly this. Whenever taking advice, particularly "free" advice, you always need to take into account the motivations of the advisor.

agreed. never work with someone who has conflict of interest with u, even if they are ur best friend. will always end up badly.

Having worked as a lender. My advise is that rate is only 1 piece of the puzzle. There are so many other aspects of loan.

Really there are three things to a loan:

1. rate

2. fees

3. features

For retail P&I homeowners it is really that simple. Investment loans a different kettle of fish.

"Service" is achieved if the 3 things mentioned above are always first rate from the lender.

What sort of service do you need? The other main difference is whether they'll lend to you at all, but beyond that "services" are largely irrelevant.

Agree. Once it's set up, what customer service do you get the values such a big difference in rates. For one there's no guarantee a major bank gives you better service.

Can anyone comment of this loan? Is it good? What's the fees like? Their website designed to get me lost.